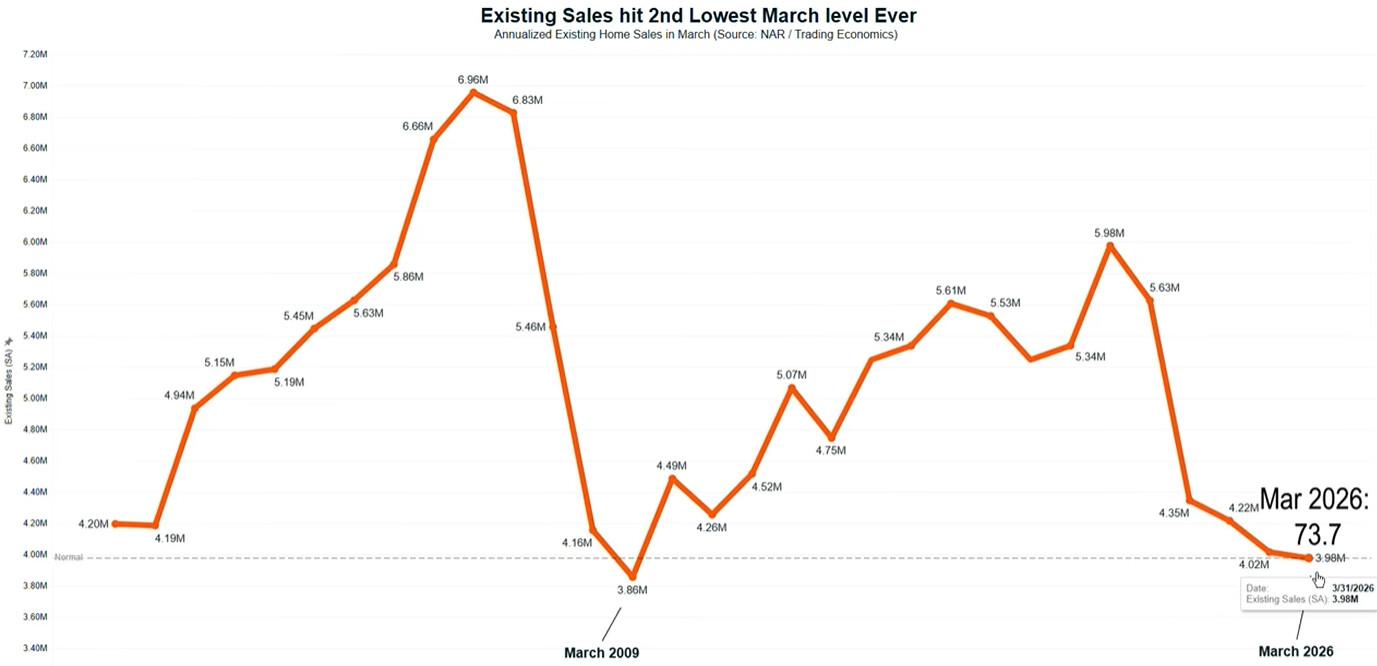

Median days on the market has been creeping up the last few years but is still well below housing crisis levels. We don’t have stacks of subprime loans. This isn’t anything like 2008, for those predicting a crash.

Housing jumped in 2022 but has only risen about 10% since 2023. Time spent at home jumped due to COVID and has remained at higher levels. None of that is reverting back to a longer term mean, at least in the shorter term. People use their homes more now than they did 20 years ago.

Subscribing to Claude Pro for work.

The web offers 17% off the monthly fee for an annual subscription. But it was giving me issues subscribing due to my VPN, so I moved to mobile.

Mobile offers 10% off - less of a discount, otherwise the same.

What is this metric? (S&P earnings / market cap) - 10YT?

Sky high valuations exist in a very small number of companies and that’s distorting the metric. That’s not a reason to avoid stocks. That’s a reason to avoid those companies. And that includes the ETFs that mirror the index.

Do you mean to avoid some ETFs? And if so, ones that mirror which index? (The S&P 500, because you think a very small number of companies is distorting it?)

Yeah, AI inflated tech is 30-40% of the index and have gone up 2-3x in the last year. You have plenty of options to avoid buying into that if you feel it is overvalued, or at least reduce it’s weighting by using ETFs like SCHD.

I moved $100k out of SPY and into SCHD last week and I think I’m going to do that again this week. Maybe not $100k, I don’t know. It feels like having ~70% of my money in SPY, and by extension a third of my net worth in a small number of AI stocks… I’m a little nervous.

It’ll do that even when it’s wrong.

Pulled the trigger on moving another $100k to SCHD. My dividends will be equal to, or very close to, my mortgage payment. Interesting.

Humph. US sells 30yr bonds at 5% for the first time since 2007.

Worth a rebalance or not?

Not even sure what rebalancing you would do? Until recently I would have thought 30 year US government bonds at 8% would be quite attractive. No maybe they should be viewed as an expectation of higher future interest rates. Even if you believe this is a signal of higher future rates, what is best portfolio to reach today?.

Tempting to shift some of the money I have in TBIL to VCLT. 3.5% → 5.86%

In the US, as a resident do you get a tax emption for holding tbills to maturity? (As in you pay no tax on the capital gain)

I added to some bond funds this week, BND, BNDX(INTL), BLV (LONG). Taking bond weighting up to 20% from 8%.

It is more than a signal, it is the current market price.

The yield curve tells you what the cost of borrowing is now, and to an extent, the price of debt going forward. You can “lock in” the price today for a loan beginning in the future.

E.G. buy the 10 yr bond and short (sell) the 11 yr bond. You will invest very little money, since the prices will be very close to each other. In effect, you will be taking out a loan starting in ten years and lasting one year for an amount exactly equal to the face value of the bond. You can cancel this lock at any time by liquidating the position.

Why might you do this? Well, if you have an expected outflow 10 years from now, such as a college education or two. If you have been planning on taking out a HELOC to finance the cost, you can lock in that cost today…or you can wait ten years and see what the rate is then.

To me that sounds a lot different than “a rebalance”

This sounds like reserving to me. Setting aside funds to pay for known expected costs should be allocated separately from your retirement portfolio. If the expenditure is 10 years off those funds should still be invested but the allocation should not be the same that you would use for retirement. Your emergency fund belongs in the same category.

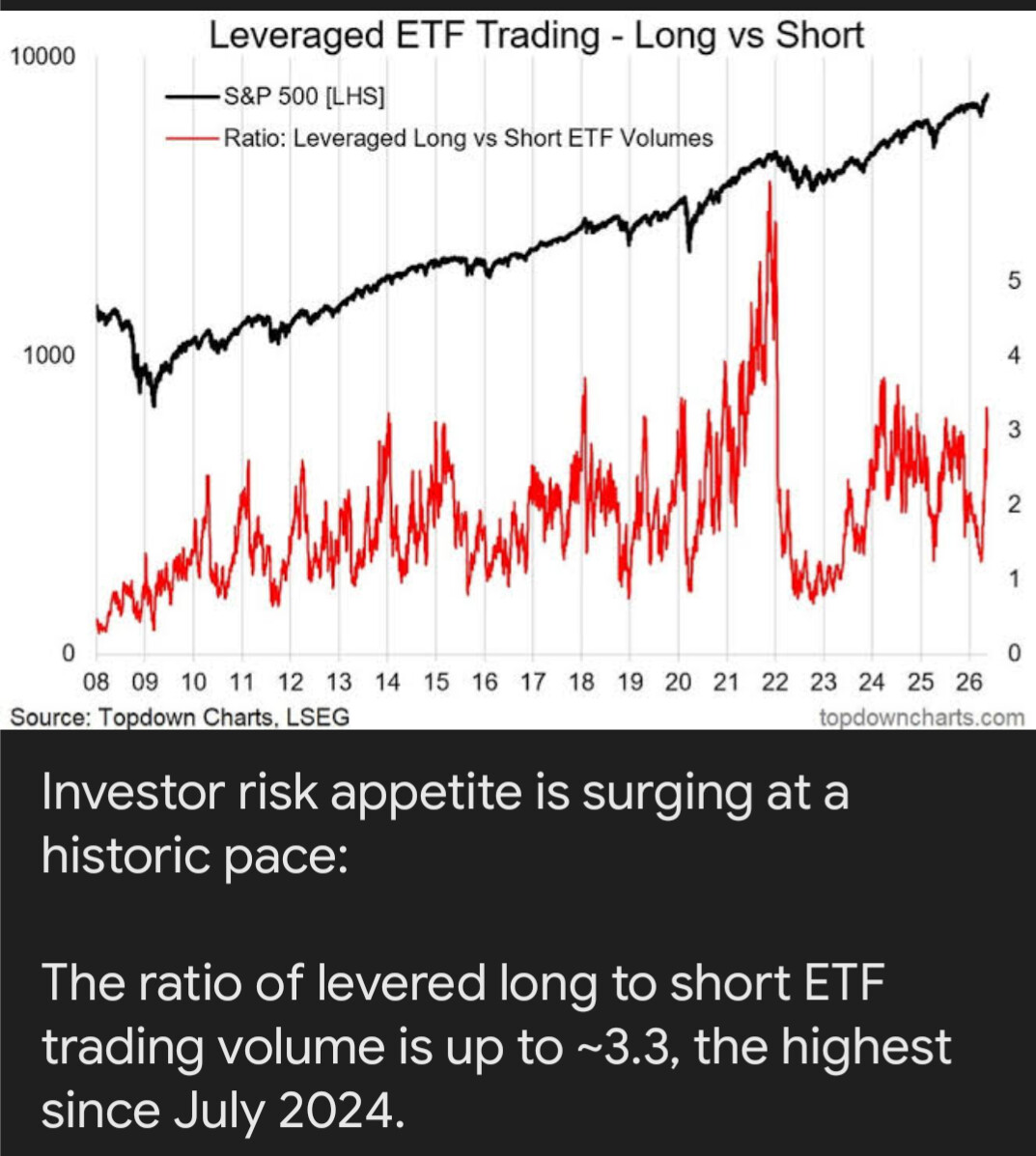

It’s an interesting chart, but the caption that it’s surging at a record pace seems a bit off