Question from someone who isn’t even up to Novice level on AI: wouldn’t AI consider the capital gains impact? Or does it not even have your cost basis available to work with?

I shared the unrealized gain/loss position in total, but I did not individual lots. It’s advice was to unwind the position over a few years and spread out the taxes. Which is somewhat conflicting advice - like if A is better than B from a long term tax efficiency perspective, why not cut over ASAP.

I assume this is a limitation of AI as actual intelligence. It’s just piecing together the most likely string of words as a response without taking into nuance. I am smart enough to ask follow up questions, but there was plenty of pretty bad info presented in this experiment.

I know it technically loses money, but I paid off my $22K mortgage last week. It no longer seemed to deserve a column in my spreadsheet next to all those bigger numbers. ![]() After today’s big day I am up $60K (roughly 3%) in investible assets this year. Not bad considering SPY and QQQ are down about 1% YTD. Having at least 1/3 of my portfolio international likely helped, VYMI and VEU and LVHI for the win!

After today’s big day I am up $60K (roughly 3%) in investible assets this year. Not bad considering SPY and QQQ are down about 1% YTD. Having at least 1/3 of my portfolio international likely helped, VYMI and VEU and LVHI for the win!

8 Likes

April 8 2025- April 8 2026 was a pretty wild period with it starting from the liberation day TACO last year. S&P was up 36%.

I’m up closer to 40% between new money in the last year and a fairly conservative brokerage account strategy (earning a spread against over my mortgage). I am completely unprepared to have another year like that.

LVHI is my large capital gain position that AI doesn’t like due to tax inefficiencies as it is not all LT dividends. I am going to leave it for now and put new money in VXUS. LVHI is a better match to back the mortgage and since I now have that covered I shift the new money elsewhere.

Same here with my 80% Asian holdings.

SK stock prices have been absolutely wild. I was up 60% in 6 months and it then tanked to 10%. Now its back up to 40%.

I am just going to wait this one out.

Congrats, huge accomplishment!

Totally understand that the satisfaction of getting rid of it is worth more.

1 Like

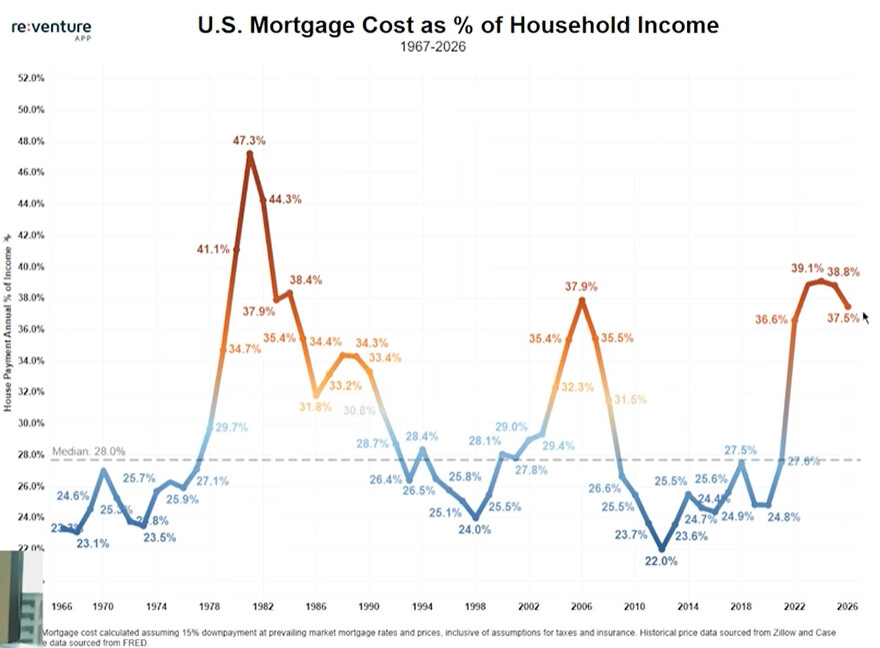

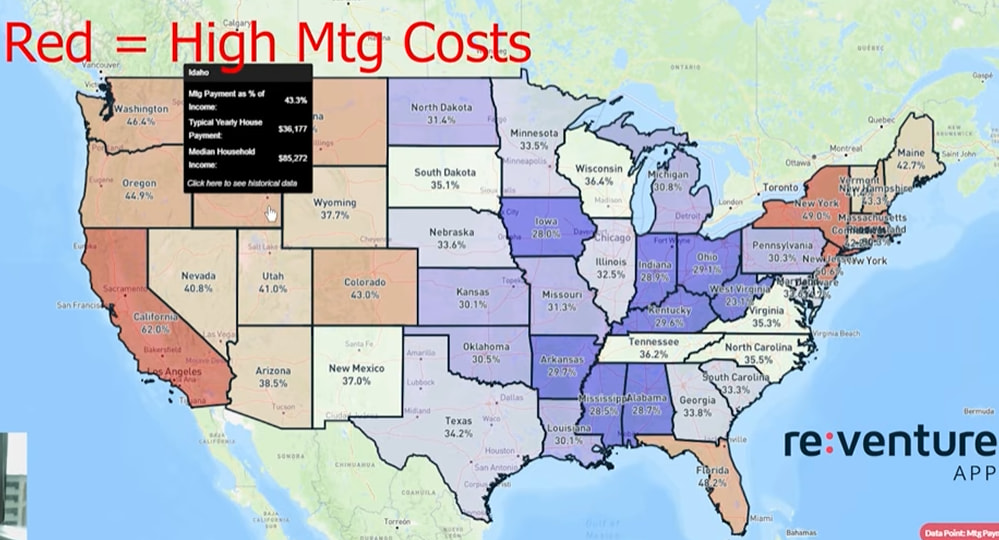

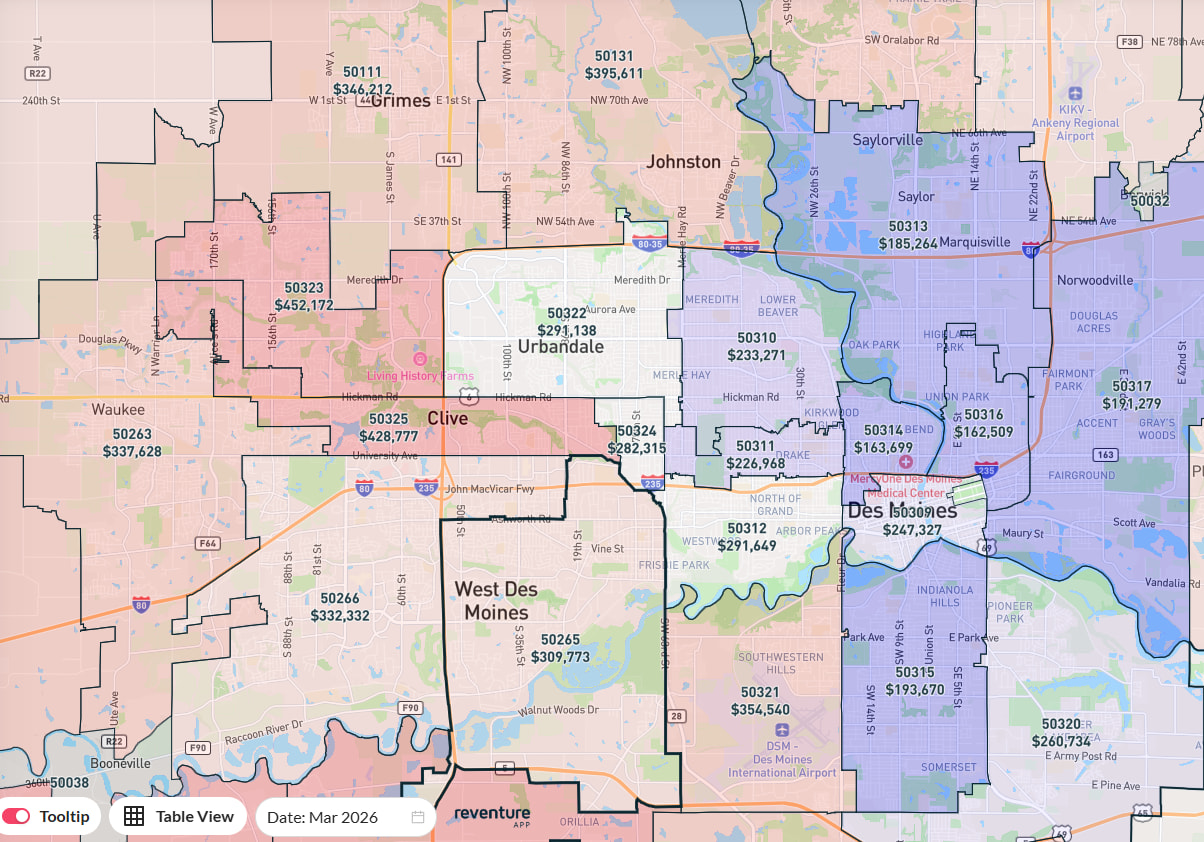

The reventure website has lots of cool graphs on housing. Some have zip-code level detail. I lifted these pics off of a youtube video. Only a few maps are free, naturally they want you to pay for more…

Locally, I know I live in one of the zip codes that has been on the hot list every year now since COVID. It’s in a good suburb where 4+ bedroom houses are common. Given declining fertility rates and 3rd kids becoming less common, this feels very WFH driver, I presume similar to West Des Moines.

Commuting costs have gone up in aggregate roughly with inflation, but there is a big savings for those who wfh worth thousands a year. They are spending this on housing, and at this point, I think this is a permanent shift.

I walk around our suburb which is about 30 years old. Seems like there were a lot more kids around when we moved here 20 years ago. Maybe more new families bought the new development. Those thirtysomethings are now in their 50s and 60s and the kids have grown up. It is still an attractive location but I suspect the young families are gravitating to even newer construction farther west and north.

1 Like

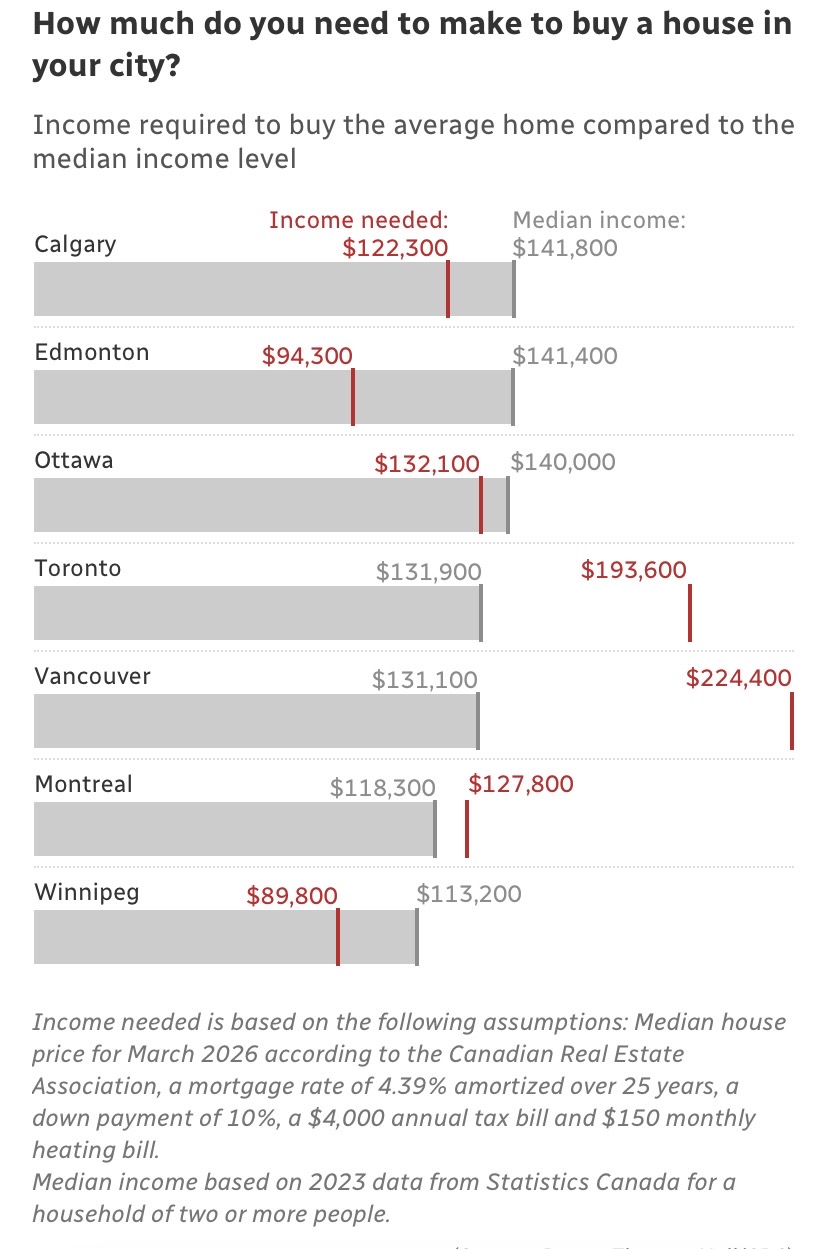

Thanks. You might find this Canadian chart on affordability of interest. Vancouver and Toronto are the SF and NYC of Canada.

Give it another 5-10 years

I live in a neighborhood of 600 homes built 40-50 years ago. Very few original owners left.

Everyone on my block has kids under age 10

1 Like

Gonna need a little more than $200k to buy a home in San Francisco in the year 2026

The $224,400 in the chart is the required annual income for the median home in Vancouver which is about the cost of a three bedroom townhouse in the suburbs. A detached house in downtown Vancouver would cost three times that amount which I assume is not dissimilar to SF? A first time buyer needs to be making $500K+ to buy a nice house here. Crazy.

The suburbs are just as bad if not worse than downtown due to companies like Apple in Cupertino, google in Sunnyvale,fb in Menlo Park, AMD and nvda in Santa Clara

basically every major Bay Area tech company is in the suburbs

I guess you can argue that San Jose housing is more expensive than San Fran

TL;DW: Your portfolio should be 100% stocks, 1/3 domestic, 2/3 international

I wish they’d do median vs. median rather than median vs. average.

Also, has no one heard of a starter home?

1 Like

I know housing is expensive in Vancouver. I struggle with this analysis where I feel it’s a bit like complaining that a first time home buyer can’t afford a single detached house in Manhattan. I think it’s less that prices are crazy and more that huge numbers of people want to live there and to sustain that you’re going to have to live in a condo or apartment tower.

My neighborhood is mostly 100-120 year old homes, and it is very mixed. Obviously no original owners, but on that long of a timeline all kinds of family dynamics must have played out. We have old folks, younger folks with kids, and a few first-time homebuyers - although not many homes here that are affordable. Just a few pockets of GI Bill homes here and there.

1 Like