Piling a bunch of money in qualified retirement accounts is great if you plan to retire at 62, but if you want to leave the rat race a bit earlier, it helps to build some up in a taxable account, although you can conceivably withdraw principal from roths or do substantially equal periodic payments etc etc

FYI: I expect SCHD to announce the results of their annual reconstitution tomorrow.

Wish Canada would update its outdated minimum distribution factors for its equivalent of US IRAs. Our factors are about 45% higher than IRAs at my age despite our life expectancies being better than the US.

I have a Donor Advised Fund, but it’s with a different brokerage. I recommend it if you regularly donate to charity. You can concentrate your donations in a single year for the tax benefit, then invest and dole it out to charities as you see fit. If you use appreciated stock to make your donations, it helps with taxes even more. There is a little expense drag, but it’s still worth doing IMO.

1 Like

Second-level reasons, there.

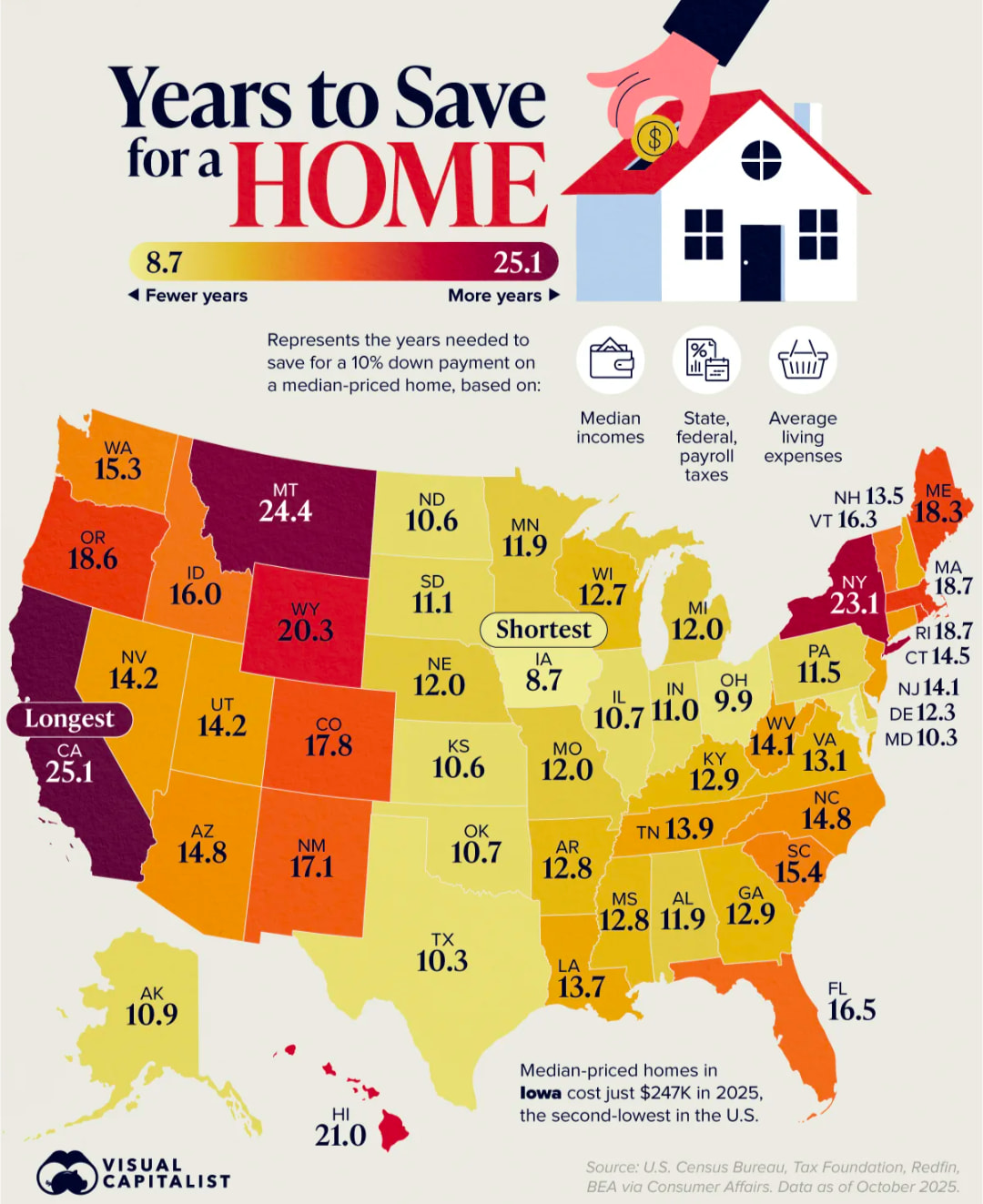

I’d think it would make more sense to use median household income rather than median income for this calculator.

You are assuming people get married then buy a home.

Surpised how crazy high Montana is. I’ve heard that Bozeman has become very expensive. Ski destinations like Big Sky, Montana and Jackson Hole, Wyoming have probably also driven up both states - out-of-staters paying big bucks while the locals earn low dollars.

1 Like

Have read about this a few times over the last few years. Locals getting priced out and its also very difficult to attract middle income folks there (teachers, social workers etc) because of the high housing costs.

The economics of a vacation rental are putting a floor on home prices everywhere.

Well, anywhere that people want to visit.

Yeah, I expect Maine is similar. Out-of-state folks buying vacation properties, driving up home prices but not altering in-state income.

So what we learned is that we should buy vacation rentals in Iowa before people realize it is a great place for a vacation?

2 Likes

No. I’m assuming a lot of people, but not all people, end up in relationships before buying homes with their partner, married or not. I’d think median household income would be across households of varying sizes and includes singles, couples, throuples, mixed generation households, etc. Just going off median income exaggerates the time required to save as it results in household expenses taking up a greater than realized fraction of income, reducing the capacity of a person to save. Plus it reduces the total amount being saved where only one person is saving the downpayment vs. multiple individuals.

Sorry, replace married with partnered. I was making a comment about the reduced rate of partnerships among younger people. And yes, they are competing with people who are partnered, who therefore have an advantage from two incomes.

Really doesn’t matter what you pick, IMO. You’re just going to change the basis and end up with the same relative differences between states.

Sure, but it reduces the time to save to something more reasonable rather than being headline bait.

I think that the people creating charts like this are mostly all about the headlines.

Oh most likely.

I had AI look at my portfolio and recommended some updates. It was pretty persistent on few recommendations even after I went through my reasoning, so I made a few respositions on Monday in my brokerage.

The biggest challenge I have is that several of the recommendations would require realizing significant capital gains, which I don’t think I want to do. I 'll keep that as a shift I can make if the opportunity comes up (if equities fall). I should be able to LIFO out about 65% of one of my positions with minimal gains if we see a 10% pullback, and shift that into its preferred long term fund. In the meantime, I will direct new money into its suggested funds.

Looks like a big rally today on the Iran news, so that may not happen anytime soon, but the good news is that I did shift about 10% from bond ETFs into equities, so timing there was good. The additional repositionings would have been mostly equity to equity ETF.