I think Dave does great here. He is good at getting tough with people who have absolutely terrible money management. For those folks, it makes sense to have simple rules, paint debt as the enemy.

But… agree with others here that beyond that, his advice is meh to bad. If you’re smart, debt is fine. Keep religion out of financial advice. He refers people to financial advisors that have higher fees and he gets a cut.

Having done my exercise and noting how life would be just fine with a lower investment return, in combination with glancing at the S&P’s glaring CAPE ratio above 40, I am inclined to add even considerably more bonds to my portfolio now. I don’t need to be foolhardy or worry about chasing yield as much anymore when conditions aren’t great, and I’m going to try to get to 25%+ bonds, currently at 12%-18% (depending on how you view investments like JAAA)

I also love dividend ETFs now and if things go really south they will lose less than other funds but I’ll probably find myself more in cash at that point.

I recently came across a financial planning tool that I think is really good. It addresses the major shortcomings of the 4% rule. It is the TPAW (Total Portfolio Allocation and Withdrawal) Planner. It was developed by Ben Mathew, who is a big contributor on the bogleheads forum.

I like that it returns a result with very minimal inputs, but can be tweaked and personalized more and more as you see fit.

I think people’s main complaint is that it requires estimates of, and is sensitive to, parameters that are hard to estimate (expected future stock market return, risk aversion factor). The counter argument, which makes sense to me, is that any reasonable planning tool will require these things. If it seems like it doesn’t then there is a good chance it is making the assumption implicitly (future stock returns will follow past returns) and it is better to explicitly make your best guess.

Ben also had a good interview on the Ben Felix rational reminder podcast, where he talks about the topic.

One of his cohorts had the temerity to go against him on it and was made to correct himself. Ramsey went on a lengthy rant against “hope stealers” after that.

Doesn’t Ramsey advocate a snowball approach to multiple debts?

So if a caller has 12k in auto loan debt at 4.9% and 30k in credit card debt at 25% interest, he advocates going after the auto loan debt first because it is smaller and therefore quicker to extinguish.

I think that’s bad advice. The best approach is to attack debt in decreasing order of APR.

Dave is the financial advice equivalent to Chime and Acorn, from my understanding of the latter two.

None of those are inherently harmful to the user in the broad strokes, and using it might mean that they’re on a correct path of paying some attention to their finances.

Both can be penny-wise, pound-foolish and are marketed to/used by toward people with minimal financial knowledge.

It’s bad math advice, yes. Dave’s approach is more based in psychology, knocking out one small loan quickly gives you a nice win and builds momentum. He’s not preaching to the crowd in this thread, lol.

I don’t agree with him on a lot of things, but he may have gotten more people out of debt than anyone else, and that’s something.

There is a similar clash between psychology and math if the buy to rent ratio was high, resulting in significantly higher mortgage payments than rent for an equivalent property. This happened in Sydney some years ago, where the stock market investment returns of the difference was higher than the house price market was going up. Mathematically it made sense to rent and invest the leftover so that you would have more equity in the house when some years later you finally bought one.

However, that requires the discipline to live frugally and invest the rest, which most (younger, including myself at the time) people don’t have. If you are paying off a high mortgage, you are forced to scrimp and save to meet the payments. You could also see the investment with your own eyes and it wasn’t this imagined dream home you were going to buy in the far-off future. So, most people were probably better off buying earlier in terms of achieving the long-term goal of fully owning a home.

This difficulty to have the discipline is where the avocado toast meme (spending lavishly while still renting) came into being.

Actuaries (in general) tend to ignore the behavioral impacts of the reasoning behind financial decisions because they will always invariably focus on the numbers.

Dave R goes the other way completely. I think its fine as it works for the people that he is targeting.

I think the theory behind the snowball approach is psychological, to get the person some quick wins so they see progress and keep doing it. If you have a large debt, progress will appear slower and you may give up and choose bankruptcy instead.

First, stocks and bonds are more expensive and have lower yields today than they did in the past. It is problematic to assume that these assets will grow at historically high rates of return when they are yielding a lot less now. To correct for this, we shift the historical return distribution down to reflect current yields.

This is where I get confused. Surely this has been true in the past (having lower yields) and then they went up again. Is it part of a cycle or are they expecting a new normal?

Perhaps there will be a new normal. The US was arguably the pre-eminent financial market in the world ever since World War I and 'we are using records mainly from that period. What happens if the US loses that position?

As I understand it, the default setup estimates future stock returns based on CAPE. So because prices are so high relative to earnings (compared to historical), they are assuming a new normal. edit: Or maybe it’s the current (not new necessarily) normal if you believe we are close to the peak of the typical cycle. Semantics?

I think that’s the point. They looked at the historical data, and when prices were high, yields came in low. And after that period of low yields when prices were not so high, yields improved.

The good news is, whenever there is a big downturn, the P/E will recalculate, and your losses will be partially offset by higher future yields. If you are early enough in your career, the loss is likely to be more than partially offset. You’d want to be able to buy in at historic lows.

And if you don’t buy into the 1/CAPE methodology for whatever reason, then you have the freedom to deviate from that assumption.

That’s interesting. So, if we retire into a high P/E market, we should probably pay more attention to what happened historically when retiring into a similar phase of the cycle - at least for the first few years. It looks like we have approximate P/E S&P data back to 1926 and the Shiller ratio goes back to 1870.

So, if we retire into a high P/E market, we should probably pay more attention to what happened historically when retiring into a similar phase of the cycle

I think that’s what it’s doing.

Let’s say you were retiring today. It looks at the current P/E and says “this looks like what a peak historically looked like.” The benefit of riding the wave up is reflected in your current asset balance. It would advise you to hold a higher allocation of bonds.

If it is a peak, you were insulated by your bond allocation. If turns out to not be a peak, then to whatever extend the actuals differ from the expecteds, the tool recalculates. In retrospect you played it a little too safe, but it was your best guess at the time. And the fact that an actual big loss hurts more than missing out on a potential big gain is already contemplated by my risk aversion and utility theory.

So all the looking back and figuring out is done by the tool. I just have to play with the sliders and parameters to make sure it aligns with my personal beliefs.

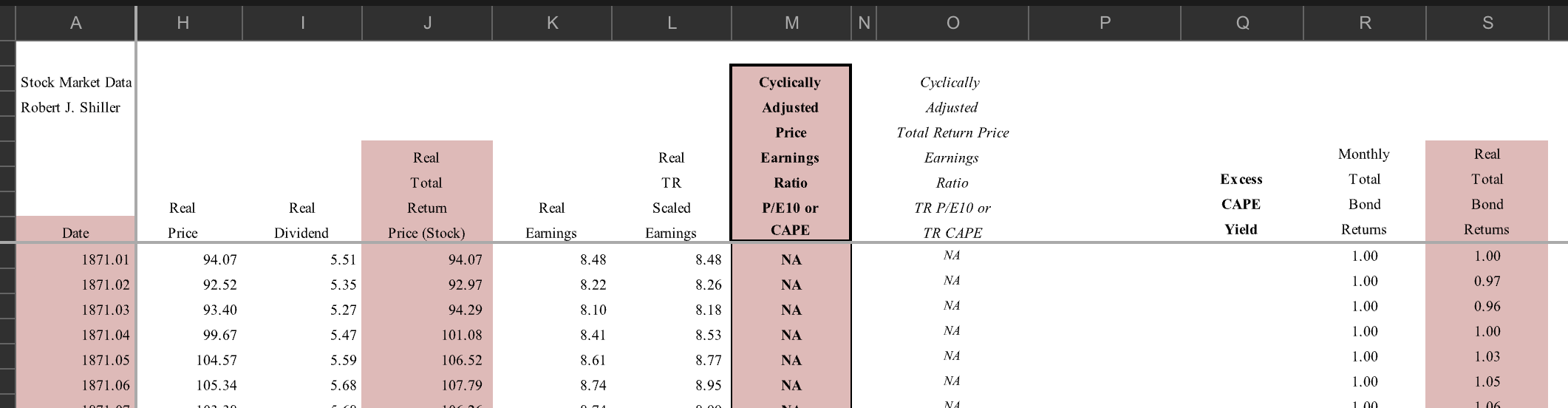

I clicked on the Return Data and then the Data tab which goes from 1871 to 2021.

It looks like column H is stocks and column J is stocks plus dividends in 2021-04 prices. Would column J be equivalent to S&P500? Also, column S looks like the total current value for $1 worth of bonds purchased in 1871 (in 2021-04 dollars). I assume they’re treasury bonds (or a mix)?

I think in the tool the bonds in the allocation means TIPS, and you’d duration match to meet your future spending assumptions.

And I think to a boglehead stocks means total market, so VT or VTI+VXUS. But I don’t know what they’re using for historical backtests.

I don’t know where corporate bonds fit into that picture.

I’m glad you’re looking into the tool. I’m definitely not the foremost expert on it, but the only way a person would follow the guidance of the tool in real life, is if they looked into enough where they felt confident in the methodology. Which it seems like is exactly what you’re doing.

This is not financial advice, I am not your financial advisor

I added the mortgage to my spreadsheet, and I went in and added a sort of lean FIRE budget. ‘Lean’ for me still includes enough for one reasonably big vacation and one smaller one (or two large ones with some credit card churning), and $6k/year as a slush fund. We are at 99% of the lean number, and my bonus arrives tomorrow to put us over 100%, so I’ve got that going for me.

Yes, I’ve reached the stage where I’m getting tired of the grind and thinking about this all the time. Maybe not super healthy.