Traveling is for suckers.

1 Like

But it’s the only way I’ll ever see Selma, California. The raisin capital of the world.

5 Likes

It was actually called “Home of the Peach”, until it was led astray. ![]()

1 Like

I didn’t ask about VYMI, as i own it, like it, and it’s well diversified.

I don’t think any of the stocks you mention for concentration risks are overweight in SCHD

I retired a couple years ago. I’m working part time making about 100-150K. Haven’t had to touch the IRA yet. Also, IRMAA sucks so I’m trying to keep the income down. Between 3 pensions and wife’s SS and my part time, we’re very close, if not over. No room for Roth conversions yet.

The trifecta of increased net worth, worsening Uber offers, and a side gig at my bridge club has caused the delivering to drop off significantly, although I will probably still do a bit to get out of the house on nice days. Running the bridge game is only an extra hour of my time, some prep before and cleanup afterwards, plus a tiny bit of extra stress playing while running the game (entering the names into the computer, collecting money envelopes (costs $10), giving change, printing out the results). But hey I won today and came home with an easy $100 ($60-$70 after Uncle Sam). Hard to say what earnings might come your way, it all depends what you want to devote yourself to. Very possible it doesn’t end up being worth your time, who knows.

As for being 20 years out, as I have probably said before I see retirement in two phases: getting to social security and afterwards. If I get $40K per year SS starting at age 62, I only need another $40K to have $80K and so I only need $1M in savings. But I also needed to fund the years 52-61. It didn’t seem difficult to imagine $1.5M staying above $1.0M over the course of 10 years, that’s just $50K/yr plus whatever investment gains and elbow grease. That dichotomy was really helpful for me to visualize how I was going to make it.

I just thought of an interesting modeling situation. Under a range of possible investment returns, what amount can I draw down each year before SS such that the amount I am left with is the amount that would fund that same amount after SS less the 40K I would get from SS? Let me break out Excel (alas if only someone out there needed 5+ hours of Excel work each week). I get half the return, then deduct the whole year’s expenses, and another half year return. Something simpler for the half-year Sure a constant investment gain is asinine but it’s just a start.

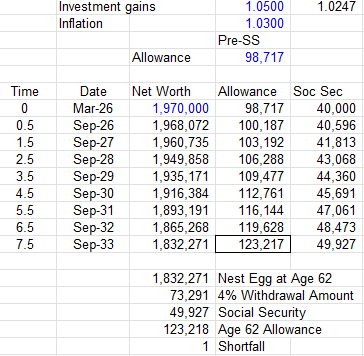

I have $1.97M. If I gain 5% on my investments and assume that my initial allowance and eventual social security payments go up 3% per year, I can spend an inflation-adjusted $98,717 each year. When I turn 62 I would still have $1.83M which is good for $73,291 of spending per year. Add that to my $49,927 of social security and I would have the same $123,217/yr I was living on each year before.

That being said I’m happy to continue living on considerably less, but having the forecast gives one some peace of mind. Keeping the 3% inflation constant and varying the investment gain we get:

0% gains = $81,033 / 2.5% gains = $89,303 / 5% gains = $98,717 / 7.5% gains = $109,356

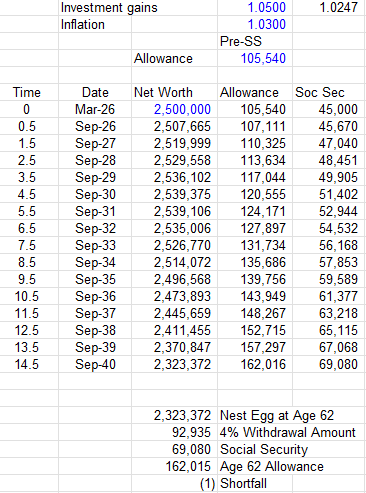

Let me help ![]() I’ve got you at $2.5M and not knowing your specifics I’ll up the SS to $45K and give you a 14.5 yr horizon (too lazy to modify things very much at midnight). Let’s put in 5% investment returns:

I’ve got you at $2.5M and not knowing your specifics I’ll up the SS to $45K and give you a 14.5 yr horizon (too lazy to modify things very much at midnight). Let’s put in 5% investment returns:

0% gains = $74,500 / 2.5% gains = $88,127 / 5.0% gains = $105,540 / 7.5% gains = $127,198

There is one disconnect here and that is the 4% rule assumes being 50%-75% invested in equities, so we likely wouldn’t be targeting 0% gains in the interim. I suppose this is just telling us what a “lost decade and a half” would do to Mathman’s situation were he to take his job and shove it tomorrow.

This example has you taking SS at 62, not your full retirement age.

Speaking of lost decade and a half, I’ll put this here instead of a different thread where it might normally go…

The CAPE ratio at 40.4 has never been higher except for the financial crisis of two decades ago. Now I remember why I don’t mind pulling out of the market at any point…

Took me a minute to figure out what you did there, that’s an interesting bit of modeling.

So, I’ve only looked at my statement, haven’t seen my wife’s. If I quit today I’d get $2,400/mo in today’s dollars at age 62. Let’s say $1,500/mo for my wife, that’s $3,900/mo and you’re pretty close there at $45k.

At any rate, I think we are perhaps closer than I’d previously thought. I think in a few years I’ll clear my bar of feeling fine on a 4% budget, targeting 4.5%, and maybe going for an extra buffer of a year or two in cash. The market is up and I’ve been saving quite a lot each paycheck!

the guy who is credited with the 4% rule amended it in the last year or so to be closer to 5%. somewhere in here is a link.

at my age, my bridge years are a short span. I am not going to be done before 62. I need to make it to 65 (medicare) and 67 for FRA and then…it is interesting to me how large the family SS projects to be. I only assume 75% of it. It’s my damn spending that is high and I need to revisit that the most

Funny. I tried replicating his study using inflation-adjusted s&p and US treasury bonds returns with a 50-50 split (adjusted annually) and the highest I could get for 1929 (the worst year) was 3.65%. Other years I could go much higher of course.

S&P I used this - Inflation Adjusted S&P 500 by Year - Multpl

Bonds - https://pages.stern.nyu.edu/~adamodar/New_Home_Page/datafile/histretSP.html (US T-Bond)

Inflation Rate - https://www.investopedia.com/inflation-rate-by-year-7253832

I started 1929 with 1 unit, multiplied that by one plus a 50/50 split of inflation-adjusted s&p/bond gain/loss for that year and then at the end of the year took out 0.0365. I then did the same for 1930 with the results of 1929 and repeated the process through the 30 years. 0.0365 finished with 0.001 left over. If I tried 0.037, it went negative 0.027.

If one could get hold of the S&P/bond returns and inflation rates that he used, it would be easy to check. It may be that the portfolio was rebalanced more often.

Yes, he is now advocating for 4.7%, assuming some flexibility. I think he created the 4% rule as a fun exercise showing that 4% is very, very safe. It was very novel work, and over the years it became gospel for the FIRE folks.

Same, man. Same. Our restaurant budget always creeps way up, I do think if we weren’t working so much we’d cook a lot more. We both enjoy cooking but get stressed out and say screw it, let’s go out.

1 Like

On rereading the wiki article on Bengen’s 4% study, it looks like his bond to stock allocation wavered between 50/50 and 25/75. It’s unclear whether the allocation didn’t matter within these bounds or if he responded to the market by changing the balance. His safe amount was actually 4.15% but changed to 4% to make it easier to remember. His 2025 book (maybe worth reading?) suggested a portfolio allocation that could up it to 4.7% (as @Mathman mentioned).

With the data I scrounged up above (which seems to understate the returns compared to his study) and sticking with 50/50, I experimented with some rules. In lean years, I lowered the withdrawal and increased it in good years. I found that instantly reacting to one good year wasn’t necessarily the best, as it may have been preceded by several bad years. I tried a 3-year rolling average (arithmetical) and had several gateways.

The numbers could change depending on individual circumstances. I set my bad year withdrawals to 3.0%. In addition, to take into account how bad 1929 was, I had a limp to the finish line rule. That is, the last 5 years of the 30 years took this 3.0% no matter how much the markets picked up. This only really mattered in 1929 and any other year there would be plenty of funds so in reality, one could spend more than that. Perhaps I could have had a longer limp to the finish (10 years?) or made the lowest rate 2.75% - hard to say.

Anyway, with my data, a 3-year average of >1% loss, I took 3.0% withdrawal,

between -1 and 2%, 3.5% withdrawal

2 to 5%, 4%

5 to 12, 4.5%

Above 12%, 5%

This is easy enough to set up in excel, as long as you can get reliable annual inflation-adjusted returns since 1929 (you may find much better data than mine) for a 50/50 bond/s&p mix. Perhaps 25/75 is even better.

I was all thrilled until someone on the Mr Money Mustache forum pointed out that cFireSim (which I have used many times) does the same thing with a lot more flexibility, but with historical n-yr periods rather than a constant rate of return.

I signed up for the free version of Boldin recently and it has similar functionality. cFIRESim is also a very neat tool, I haven’t played with that one in a while.

I ran the math, with and without the equity I have where I work now. Without equity we’re at 87%, with equity (at half of the most recent valuation) we’re at 97%.

For my larger budget, at 4.5% I’m 88% funded without equity, 99% with. So, it all comes down to the IPO. Now, I never thought I’d be this close this soon, so I never included the mortgage because I figured it wouldn’t really matter by the time I would hit my number. So in reality I’ll need about an extra $100k, I owe $148k but I’m getting a ~$30k bonus in three days, plus whatever else I pay off in the next year. If we IPO at a big number, I could pay off the house and be really close here.

Also note that while I’ve tried to build a pretty thorough budget, my wife has not yet done any QA to tell me what I’m missing or what I got wrong. But I have $10k for travel in my ‘base’ case and $15k as ‘ideal,’ plus an $8k-$12k annual bonus that would act as a slush fund for things I may have missed elsewhere, things like unplanned expenses, I’ve got some wiggle room here.

Dave Ramsey is pushing taking out 8-10% a year. Totally safe since the market grows at an annual rate of 10-12% /s

1 Like

Dave Ramsey is popular on TV/Radio/Media because he’s opinionated, outspoken, and surprisingly consistent. But he’s only right about 75% of the time, IMHO.

He hates leverage. OK, I get it. Most people borrow too much and spend a lifetime paying off loans of all types, student loans, car loans, credit cards, mortgages, boat loans, etc, etc, etc. He’s correct to hate them, but I am not paying off my early my only debt, a 3.25% mortgage taken during the pandemic. Some very judicious use of debt is acceptable.

He doesn’t understand life insurance, so he hates on it every chance he gets.

He also brings his religion into secular financial topics, which I find offputting.

He is against prenups for religious reasons. That’s a completely stupid stance.

A 10% withdrawal rate will bankrupt the pensioner eventually. He lacks the math skills to know and work with the fact that a long term stock market yield of 10% is NOT THE SAME as it always returns 10% each and every flipping year.

After thinking about a withdrawal rate for years and years, I am comfortable with a 1/280 per month rate. That’s an annual rate of 1/23.33, or about a 4.29% annual rate - but mentally my math is a monthly rate.

4 Likes

I’ve only listened to him a few times, and most of the calls have involved this theme with people drowning in debt. He gives good advice on that, so most people benefit from the dose of medicine he gives them. I agree with you that some of his advice is very wrong, and 10% withdrawal rate advice certainly falls in that category.

CAPE and other measures indicating that stocks are overpriced have been high and going higher for quite a while. This is a big reason why I’ve been moving assets to dividend payers. The dividend payers have much lower ratios. While many of these companies are probably overpriced, they are at much less extreme valuations than some of the market leaders. If things fall apart, I expect that my dividend portfolio would fall half as much as the broad market. I get a measure of safety for my portfolio while still keeping some growth.

I like to say that it’s hard to hurt yourself too badly falling out of a first floor window.