Public debt is probably crowding out private lending that could be more useful than giving a shit tonne of money to Argentina…

It looks like this discussion took a sudden turn. I’m going to respond with two posts on two different topics.

I haven’t been talking about eliminating the debt, I’ve been pushing on your assertion that …

But the fundamental truth is the interest expense takes two numbers to calculate, and the Central Bank has pretty much a free hand at setting one of them.

You said the the federal gov’t could cut its interest payments as much as it liked by only borrowing with 3 month bills, then imposing a low rate on those bills.

I’ve said the the Fed can put a floor on short term rates, but not a cap. If the Treasury sets a dramatically lower rate on those bills than “the market” wants, then it won’t be able to sell the volume it needs to sell.

You said that the Treasury can force primary dealers to buy everything it wants to sell. I said that if the primary dealers can’t at least break even on reselling, they will decide they don’t want to be primary dealers.

In the end, the Treasury relies on private parties, some of whom can choose to take their money elsewhere. Therefore it does not control the interest rate.

I think that disagreement is still pending. Your most recent post a takes up a different topic that I’d like to follow.

Not entirely. I think fiat money ought to be better than gold. Our accounting shows the amount of fiat money as “debt”, which seems correct to me. So the gov’t should have some debt.

I agree that the amount should grow with the real economy. Further, I agree that’s complicated because velocity also matters and velocity is hard to predict. For consumer spending, that comes down to consumers’ subjective opinions on “How much money do I have available to spend?” and different consumers can have widely different ideas on the answer.

I’m sure you understand what I learned about “money”. We can pretend that the only way the gov’t puts money into the system is printing greenbacks. Banks expand the money supply through fractional reserve banking. Consumers perceive their checking balances a “money” even though the bank isn’t holding greenbacks equal to those balances. (and, it gets more complicated – what about money market mutual funds, or the credit limit people see on their cc statements?)

But, when the federal gov’t sells a ten year bond to an insurance company, it sucks greenbacks out of the economy. The greenbacks it creates so it can spend are exactly matched by the greenbacks it destroys when it borrows from private parties.

It’s clear that the MMT people take a different turn there. I’ve never pursued the rationale. As I’ve mentioned, I’ve seen “Deficits don’t matter if current inflation is low. If it ever goes up, the gov’t can easily stop it with fiscal policy”, and I’ve expressed my opinion on “easily”. But, I assume there is more there, I’m just not seeing it.

You mention “We need that spending/velocity.” regarding forgiving student loans. I’m not sure of the “need”. Maybe there is a belief that there is a fundamental mismatch in modern economies such that they can’t operate efficiently if taxes roughly match gov’t spending. I’ve never seen a debate about that proposition.

quite the assertion. but no evidence. And my lived experience is quite the opposite.

In today’s financial system, treasuries have the tiniest bid/ask around. They are liquid. Even more succinctly, they ARE liquidity. Get out of line by even 3 bps and you will get arbbed. The vultures will pick your bones clean.

All treasuries earn the short rate over the short term. That IS the futures market. That IS the repo market. So what sort of financial system are you imagining?

No,No,NO. Insurance companies buy Treasuries from a dealer. That dealer has an account at the fed. Nothing is sucked out of anywhere.

Either the insurance company comes to a deal/price on a 10 year bond or it doesn’t. That insurance company must have some explanation for why it wants that particular bond, That reason is unlikely to be “because it has a lot of yield”. higher yields than treasuries are readily available. Most likely answer will involve “we need the liquidity” at the BD. Those Treasuries allow the traders to borrow at a collaterized rate when they want to buy something.

I understand that. The fact that the secondary market is very efficient isn’t related to the the price/yield the Treasury gets on the initial sale, which determines the Treasury’s interest cost.

The market was liquid when 10 year treasuries were trading at 1% and equally liquid when 10 year treasuries were trading at 5%. (or when 3-month were virtually zero or 3-month were 5%) New 10 year bonds issued when the market was at 5% cost the gov’t about 5% every year until maturity. New bonds issued when the market was at 1% cost the gov’t about 1% every year until maturity.

And the insurance company has an account with a bank that has an account at the fed and some digital stuff happens that increases the dealers account and decreases the insurance company’s bank’s account at the fed (and also the insurance company’s account at its bank).

I don’t see any different macro economic effect than if we lived in a world where the insurance company had some greenbacks in the bank’s vault, the bank sent the greenbacks to the dealer’s vault, and got the right to collect interest and principal from the Treasury, where that right had been owned by the dealer hours or minutes earlier.

My point is that the insurance company had to get those greenbacks somewhere. The ultimate source (in a world of physical fiat money) was the greenbacks that the gov’t printed when it bought something from a private party.

Those greenbacks found their way through the private economy to the insurance company, then to the dealer, where they replaced the greenbacks that the dealer sent to the Treasury a few days earlier when it bought the bond.

For this discussion, I don’t care why the insurance company wanted Treasury bonds. My only point is that (the way I learned this back when the prof was scratching this out on the cave walls) when the Gov’t borrows money from private parties, it takes greenbacks out of the private economy. The gov’t can incinerate them if it likes. They are no longer circulating and being used for food, clothing, etc.

We no longer put greenbacks in armored cars and move them between banks and the fed for this type of transaction. But, so I was told, the economic effect is the same.

Others may be getting bored, I will respond via DM. If anyone else has a question , I will respond

Does my point about bank reserves being only two years of deficit spending have any bearing on demand for treasury auctions?

I am not aware of any hard cap for member bank reserves.

That said, The crediting of Bank reserves with interest is recent. In the past. Those moneys did not get credited any interest prior to 2008. I put up a graph on Oct29 that shows when this occurred. You can see the rapid rise of total bank reserves since that change.

From the perspective of the member bank, this is welcomed news. A bank’s ALM objective is to target as small a duration as possible. And nuthun is smaller than a daily FRN. (bank loan facilities are monthly resets; adjustable mortgage kinda structure.)

This shit is sooo complicated. But its what seems to happen when you set rules by committee.

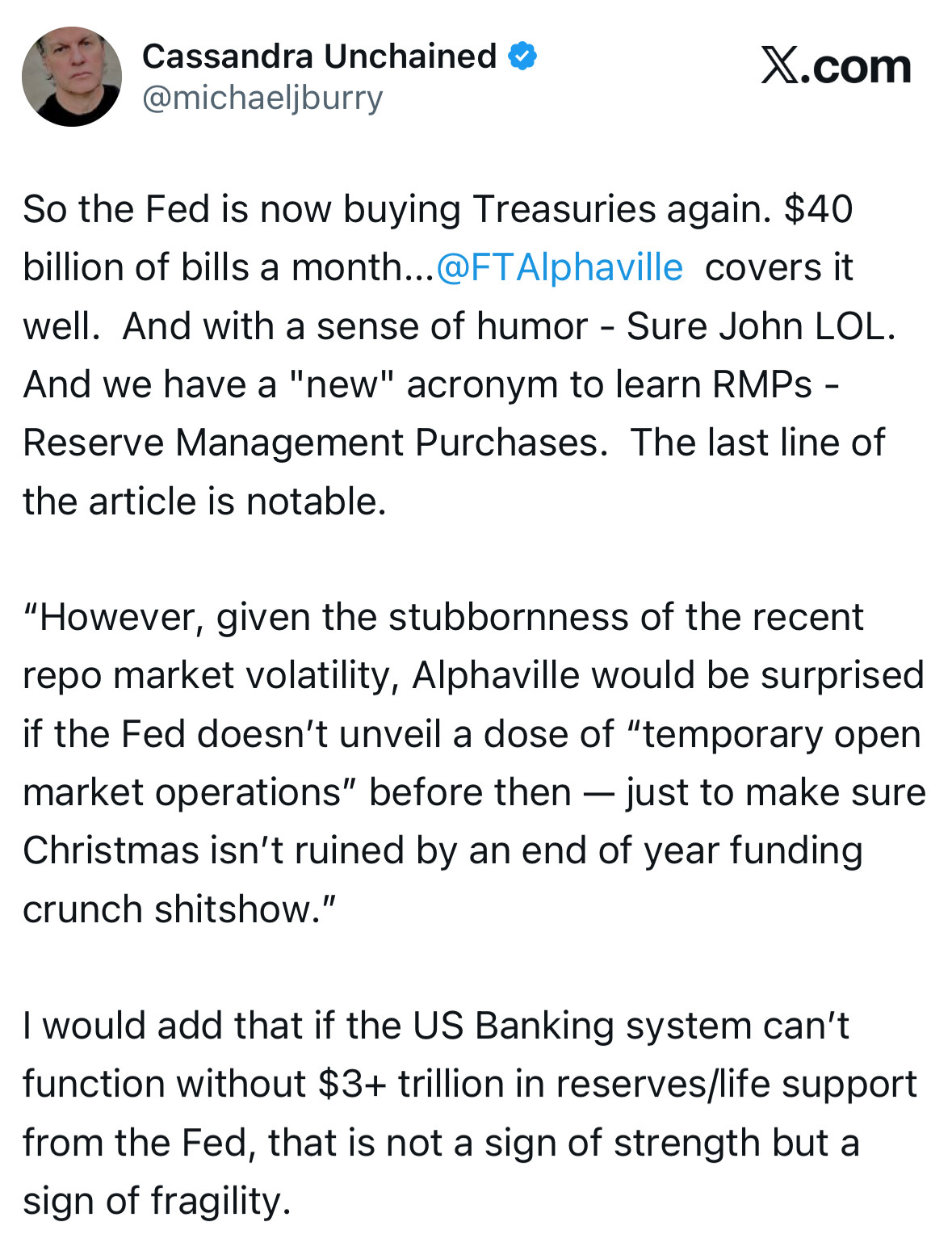

Buried in the Fed decision to drop rates was this little nugget:

QT is over.

QE is back in to the tune of $40bn/month (half a trillion/year)

They are starting to monetise the excessive deficits.

Good luck bringing inflation down with that program.

1 Like

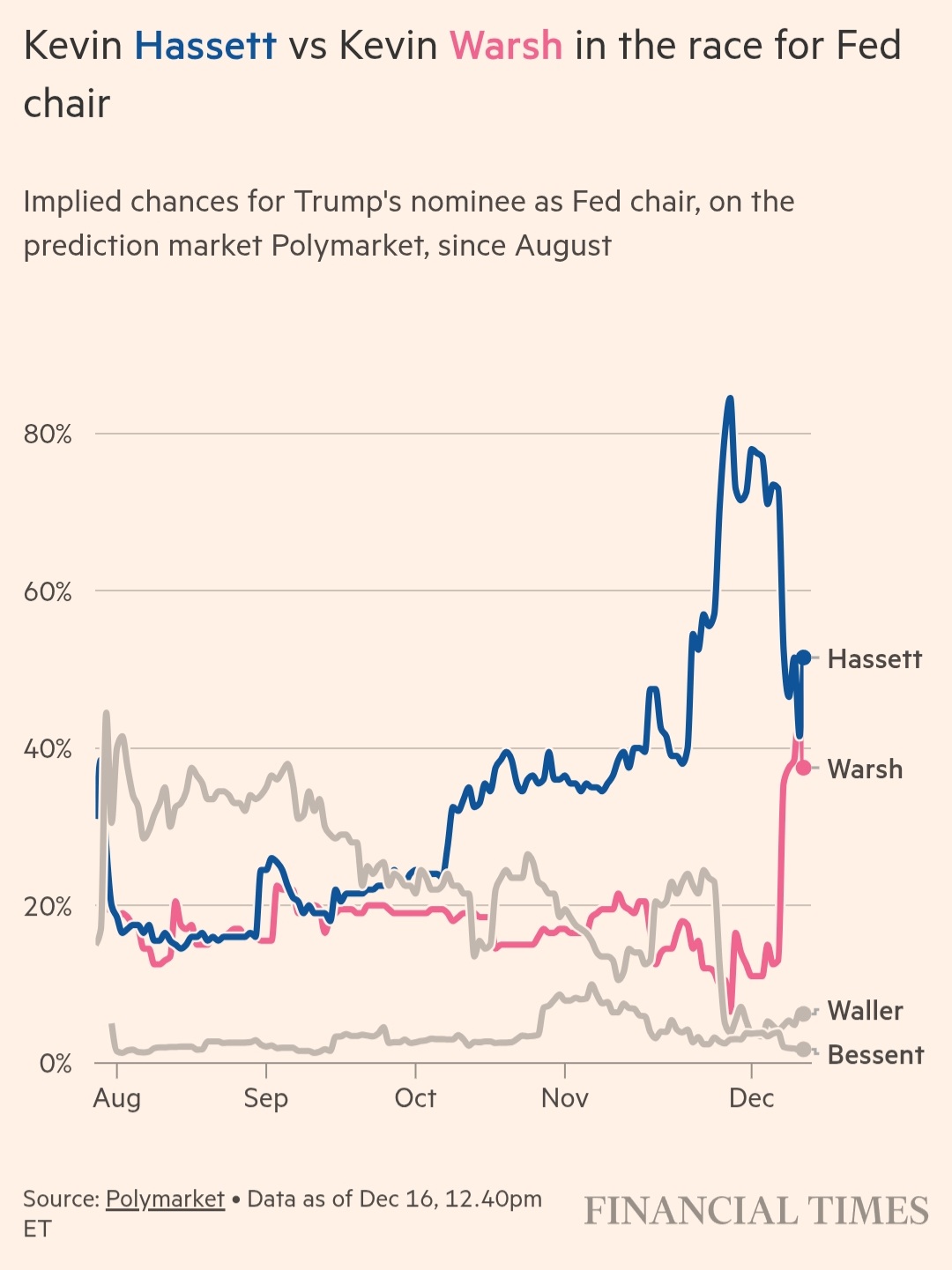

Looks like the market is finally starting to put up massive red flags because of the combination of Hassett and Miran (a bonfire of incompetents basically).

You can never tell with Trump (as he cares more about loyalty than competence) but it does look like Warsh is going to be the likely (saner) pick now.