i own a home I rent out. when we moved into the current one, it was 2007 and the market tanked and we were upside down. so i became an accidental landlord on this “starter home.”

i get 1-3 calls/texts/emails a week from some group that wants to buy my house for their investment group. it’s all different numbers, so I don’t know how many groups there are. but it is more than a few.

the investor groups have all cash/no contingency offers with closing on whatever schedule the seller wants - sellers are going to prefer that certainty more often than not.

if those groups are bidding on starter homes (to flip and/or rent) then that’s competition for those homes that I don’t think I had to compete against when I bought that home in 2001.

These numbers are interesting but without knowing the inflation rates, it’ may only be explaining hardship in the first handful of years. In periods of high inflation after a few years, a fixed mortgage becomes much more affordable compared to salary. Admittedly, if the first couple of years are going be really tough to get through, the bank probably won’t give you the loan.

For example, if the mortgage was fixed and median salary went up with inflation, a 1984 mortgage by the end of the 10th year would go from 52% of the salary to 31% whereas a 2006 mortgage would go from 44% to 37%.

That’s why median salary compared to median home price is seen more often. It captures the affordability for the duration of the loan.

Picking a single expense category is also a bit of cherry picking in its own. Set aside any criticisms of CPI itself for a moment…CPI should reflect a basket of expenses for all costs of living. If your real wages are approximately flat, and housing became a larger share of expenses, this would suggest you should see a savings offset in those other categories.

Housing is an easy target since it is the largest expense. But that also makes it one that can absorb an increase in wages.

Yep. That’s pretty important in the “affordability” discussion.

I certainly considered likelihood of future raises when we bought the house in 1981. I had been an actuary for 5 years and thought I still had some career advancement ahead, and I was living in a period of high inflation. (But, there was no guarantee that wages would keep up with prices.)

I bought my current home in 2010. I am not sure what the bank would have loaned me, but they were OK providing a letter to secure the home I wanted. This was shortly after the financial crisis, so perhaps some lenders were avoiding giving out that sort of pre-authorization up to a full limit.

Regardless, the early years were tough. I had discussed with my (now ex) about how we could make it work as long as we stuck to a reasonable budget, and that in a few years it should be no big deal. Of course, most of that was ultimately ignored.

Seems the consensus is all about inflation. But I don’t buy that. Inflation has been higher than a target rate of 2.5%, sure. But it isn’t anything like double digits for years.

I look to other policies. Top of the list has to be healthcare. Huge driver of personal bankruptcy, and a per capita cost way out of range for other countries. It gets worse every year and it’s about as close to a necessity as you’re ever going to see.

Next is energy. Costs per KW-hr have risen dramatically in the US like 300% over the past 5 years. And since there is not a single US manufacturer of transformers left in the country, that wont be addressed in any meaningful way for a while.again, a virtual necessity.

But while there are ample countries in the OECD that do better, the US is marching exactly in the opposite direction. Repeal anything Biden did on those fronts; cut HC insurance subsidies, and tariff stuff we need to import. Things gonna get worse for a while.

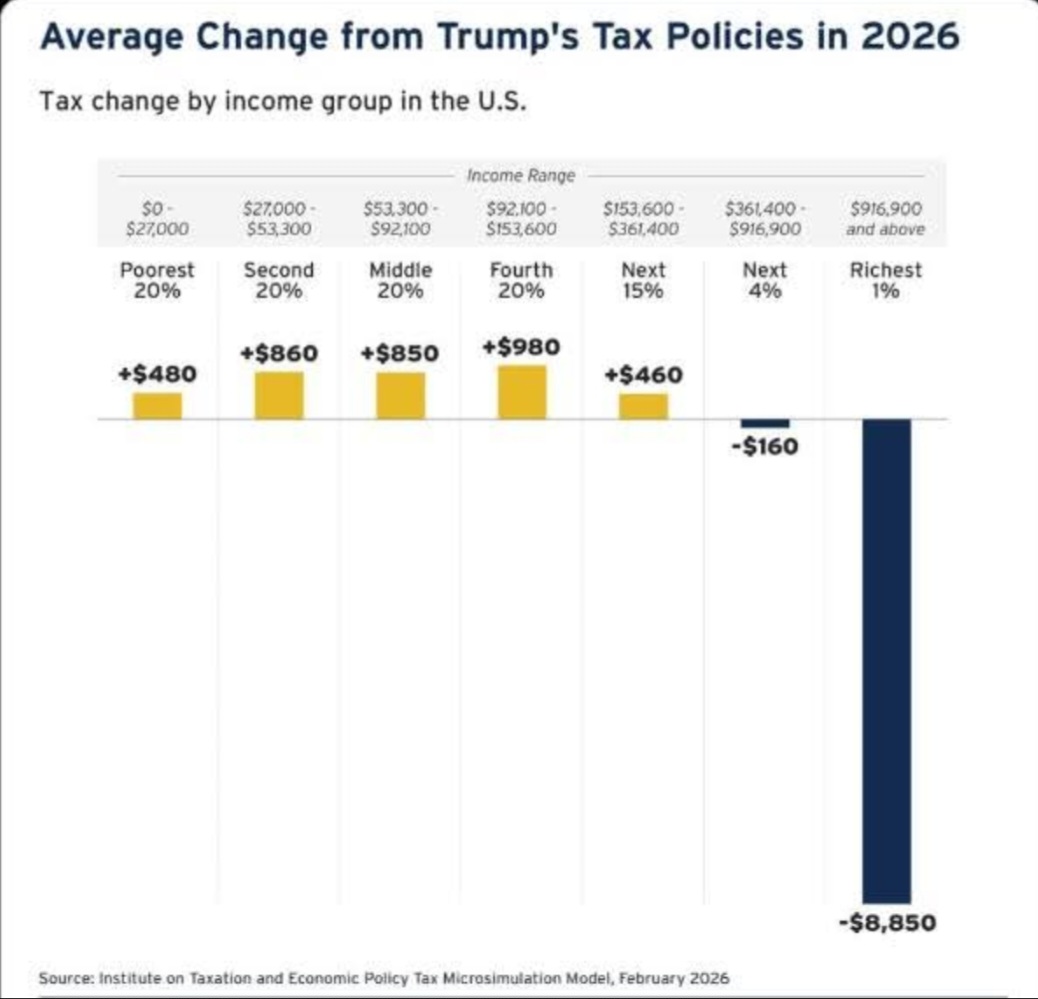

I saw a 4-5K or tax benefit from the increase in the SALT deduction cap for 2025. That is mostly a reversal of a change made in his 2017 tax bill that for me at the time ended up being fairly neutral.

The deduction cap increased 30k (10k->40k), so anyone with a higher income in a moderate to high tax state would have seen up to 30k*(32%-37%) reduction in taxes.

I was seeing some reporting that Trump went after Democrats on their claims that affordability is an issue in the SOTU. I see a lot of posts across social media complaining about affordability. Telling people they’re wrong about the fact they’re struggling with affordability doesn’t go well in elections.