Some of those comments are a bit misinformed.

SpaceX can absolutely be a bubble right now, but since its not in the S&P 500 its all a bit moot (for now).

Also, why expose yourself close to 100% to the US…

That is incredibly poor risk management, specially when you are very near retirement. Stop buying the S&P 500 index and diversify away internationally. Nobody is forcing you to buy any investment. Its a choice.

People in the US have a whole plethora of investment options and tax advantages (far more than most other developed countries) so I am always a bit puzzled as to why only a small % take advantage of their full options.

The dominant American investment philosophy is heavily conditioned by the last 18 (or even 36) years during which the American stock market has really destroyed the rest of the world.

Now when we take a reasoned look at history, we can know that nothing lasts forever, but the quiet voice saying “this time is different” will have more sway with many. Even many seasoned analysts are saying that International, bonds, small caps, hard assets and other forms of non-S&P 500 diversification are not needed.

There are a couple of reasons.

First: Education in financial literacy in the US is not great, from the perspective of “common education that everybody gets”. In high school, I had a one-semester class that focused very basic things like how to write a check (I went to school in the dark ages), how to build a (simple) budget, an introduction to the cryptic acronyms on deductions from your paycheck, and how to fill out a simple tax return.

I think there may have been a chapter on the stock market…but I was going to school in the 'hood at that time. Practical lessons on what you needed to know about cashing your paycheck, and how to get and use money orders would have been more useful.

(Actually, come to think of it, we DID cover using money orders.)

Second: I think the US has too many options in terms of tax-advantaged savings plans.

Most people in the US make considerably less than actuary money, and many/most of the tax-advantaged savings vehicles have restrictions on what they may be used for, or when they might be accessed. Given the uncertainties involved in some of the accounts, and the limited amount of money such people have available for savings…the advantage of having multiple options is quickly eroded by the perceived cost of learning about them and figuring out how best to use them in one’s own circumstances.

I’ve long thought that Americans would be better served by having one (possibly with a Roth variant, for a total of two) generic tax-advantaged program that was more flexible in its uses.

I agree. When I look at the differences, they don’t make sense. They differ depending on whether you are self employed or an employee, and whether you work for a private sector employer or a government.

Agree with pretty much all of that. Your HS class is wayyyy more info than I got back in the early 80’s. I don’t really recall anything about finance stuff, except maybe the occasional word problem in math class about interest rates. Nothing practical anyway.

Our tax system is far too complex, and it’s by design imo. It seems like it’s just multiple ways for people who already have plenty of money to avoid paying extra taxes. Most folks don’t make the kind of income to enable them to max out contributions to multiple IRAs and backdoor Roths and whatnot. Kudos if you can do all that, but it’s not really beneficial for most people.

The class was officially the semester of economics required by Tennessee for graduation at the time. However, the teacher…really nice lady, but I don’t think she had academic knowledge of economics or finance.

To her credit, she focused on the practical knowledge that many of the kids in that class (economics was only offered as a “regular” class at that school; at that time there wasn’t an “honors” version for the college prep kids, and the school wanted to have some classes where the college-prep and AP kids were mixed in with kids in the “regular” and remedial tracks – some friendships were made and informal tutoring occurred), were going to need as they started trying to earn a living and support families after…or in some cases before…graduation.

A less cynical view is that we use the tax code to incentivize behaviour rather than have outright policy for it. This results in a lot of tax dodging behavior…most of this I find associated with “small business”.

I used to have that view too.

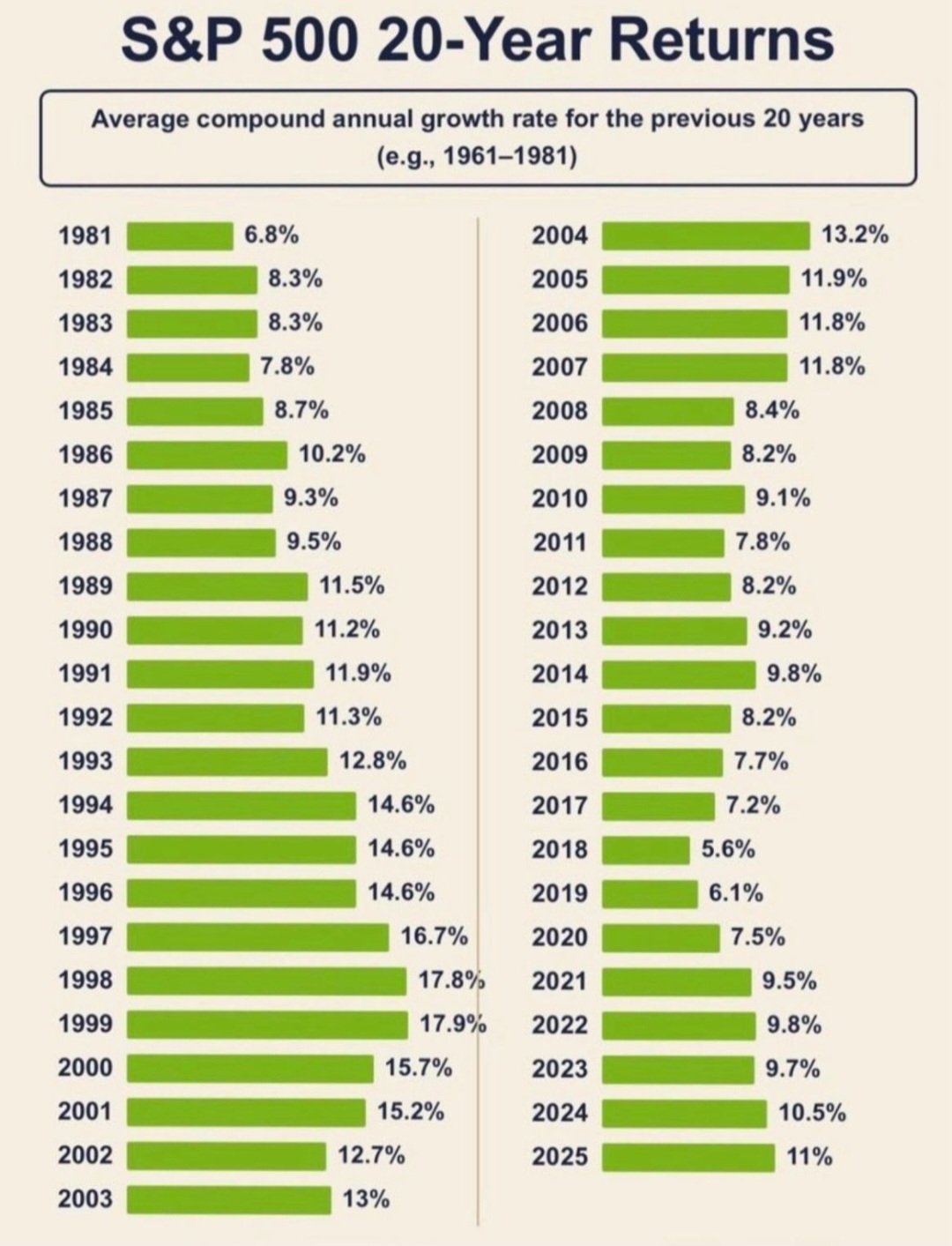

Sure. Here are the 20Y compound returns for the S&P 500 from 1981 to 2025

If you retired around the GFC while being 100% exposed to the US, you would have taken a fairly big hit at the portfolio level.

So while I don’t see a GFC in the horizon, you can see that the overall 20Y shape of the compounded returns dip quite a bit during recessions.

Adults have nobody but themselves to blame for their financial illiteracy. People are already taught reading and math skills. If they can’t combine the two skills to pick up new material as they need it in adulthood, that’s on them.

There’s a lot of people not making “actuary money” that aren’t thinking past how they can get by day to day. If you have a family and make less than $50,000/year, which describes a lot of people, it’s not surprising that you don’t have that much saved.

That’s not denying that there are a few people in the sub $50,000 income bracket that managed to accumulate substantial savings. Some of this goes back to education, but there are other factors like luck, personal priorities and family needs.

Even the smallest return in this chart would provide about 150% total return over the 20-year period. This has been enough to reinforce the idea that the USA is the only place to invest.

Don’t forget about the differing inflation for those time periods. For instance, the S&P return from 1961 to 1981 of 6.8% is barely above the average inflation rate for that period of 5.72%. It would be more useful to see the inflation-adjusted returns for each period.

Its like printing money at this point…

I suspect that when (not if) the Fed is forced to raise rates in the US to counter inflation it will start the domino effect of mass sell-offs in US equity markets.

Hard to tell when that will happen in 2026 though. Also, there is the political angle to consider (Trump will go ballistic and go after Warsh).

If our Glorious Leader still had his mental capabilities, or if his cronies were more competent, I would expect that BLS would start reporting more benign core inflation numbers.

I am more worried about the coming private credit debacle interacting with rates going up.

The deeper I investigate private credit in general, the more I am convinced its going to tank. The amount of financial emgineering going on right now to try to kick the can down the road (to not have loans default) is astonishing. There is no way that lasts if rates go up.

Now that will cause equity markets in general to take a big hit.