If Robinhood isn’t your thing, there are other brokerages with transfer offers available. Webull also has a match, for instance. Here is a roundup of current bonus offers from Nerdwallet:

Best brokerage bonuses: Realistically earn $300 - NerdWallet

If Robinhood isn’t your thing, there are other brokerages with transfer offers available. Webull also has a match, for instance. Here is a roundup of current bonus offers from Nerdwallet:

Best brokerage bonuses: Realistically earn $300 - NerdWallet

Fuck, Robinhood doesn’t do mutual funds. I’m not selling my entire brokerage and taxing tax to transfer it over.

I’ll be happy when I can move the IRA back out of Robinhood.

My first thought was why are you using mutual funds. But if that’s what you have in a taxable account then I understand not wanting to realize the gains. If the funds are in a tax shelter you can do almost anything you could want with ETFs.

I believe when I started investing in these (>10 years ago), fractional ETFs were rare or nonexistent, at least for retail investors. I didn’t have a particular need for an ETF and was investing often more than I was investing big, so a mutual fund made sense to me as an early 20s neophyte.

After the >decade of buying the same 2 VXUS/VTI funds every 2 weeks and only selling part of it 1 time when purchasing our home, it’s been easy to just throw money in and check occasionally.

I hear that, but you’ll have nearly identical results and more flexibility going forward if you switch new contributions to ETFs. For example, you could use VTI and VEA ETFs in the same way that you have used VTI/VXUS in the past.

Yeah. You’re probably right. I should let those mutual funds just chill and switch new contributions. It’s just been an easy set-and-forget account and has been nice to watch one balance grow. But I ought to switch before next contribution.

Got an alert that my 3% gold card is available. They make you commit to an annual $50/yr gold subscription (supposedly crediting you for wherever you currently are) and i don’t mind that for now as I think I have gotten some IRA contribution matching as a benefit. My regular card was a Citi double cash 2% but I like the idea of getting 3% back.

It does involve downloading a Robinhood banking app and I’ll have to see what is involved there. I’m not against some banking stuff although I hardly need another account in my life. But I think it will basically be set it and forget it.

It is available for use in my phone immediately even though the card won’t be here for some time.

I’ll be happy to put it to good use … as soon as I’m done earning United bonus miles. ![]()

I am STILL in the queue to get the RH card, I signed up early, or so I thought. I plan on cancelling my Chase Sapphire Reserve, not with it now that I don’t travel as much as I used to.

It’s pretty annoying to get off of the waitlist

best bet is just plop $1M in Robinhood and ask your plat desk rep to get you a credit card

I hadn’t looked into the card until yesterday, but quickly applied.

I’ll take 3% on everything. I never remember to follow the rotating 5% categories on the card that has that, anyway.

Do I need to put anything into RH to get the card, or can I just build up the rewards balance there?

I moved all my taxable brokerage over to Robinhood to get a ~$5,000 match.

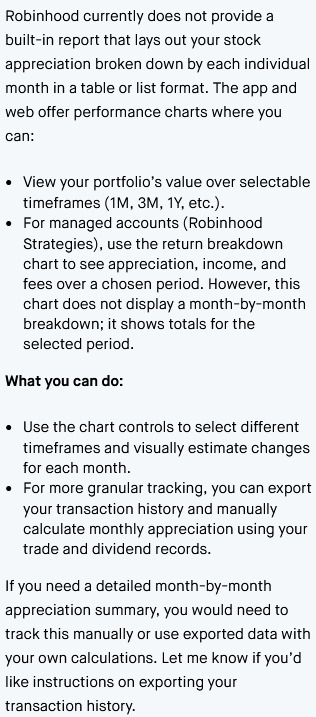

I think I’ll get over it, but I almost regret it. I had a clear, legible history in Vanguard showing balances by month, gains broken down by various kinds, etc. extending back over a decade, easy to filter to specific timeframes or group holdings, etc.

Robinhood will show me 1D, 1W, 1M, 3M, 1Y, Total gains for one holding or for the total portfolio. If I dig through their various statements I can piece together some information, but not as much as Vanguard showed plainly. I dislike how much Robinhood takes information away from the user and pushes products like a video game.

I’ll still take the credit card and $5,000 though. I have a note for April 2031 to transfer out of Robinhood.

RH seems a bit like a gambling platform from what I have read. I don’t have a known gambling problem, but TBH, I could totally see getting sucked in to something once I created an account. In fact, I was just thinking “why not use this instead of my AMEX card, take the 3% rewards and play with options on RH” since that is what it seems to be made for.

Probably a terrible idea, and I should just stick with Schwab where I can make just moderately bad decisions on buying individual stocks until I re-learn to stick with ETFs.

Right - they seem to gently hint with their UI that you should wander into playing with options and crypto and individual stocks.

Just throw my money into 1 of my 2 money gardens, please. I’ll be back in a decade.

And maybe open a margin account, or bet on sports, or oil futures. I like how easy it is to use the app, but if you’re a gambler, I think RH could be dangerous.

Oh gross. I saw they had “Robinhood Legends”, which says it’s a “more powerful trading platform”, so I was wondering if it could give me a month-by-month breakdown of my historical balances.

Absolutely not. It’s just a gamified interface for day-trading and buying options. Still doesn’t have your actual performance history available except for a few predetermined ranges.

I decided to try Robinhood’s AI “support” in case I was just missing a way to see how my investments had performed:

Their solution is “eyeball it from the charts or track it yourself”

Thanks for the free cash Robinhood, but counting down the years/months until I transfer everything out. I don’t regret it, but I liked having my >decade-long history in Vanguard clearly laid out.

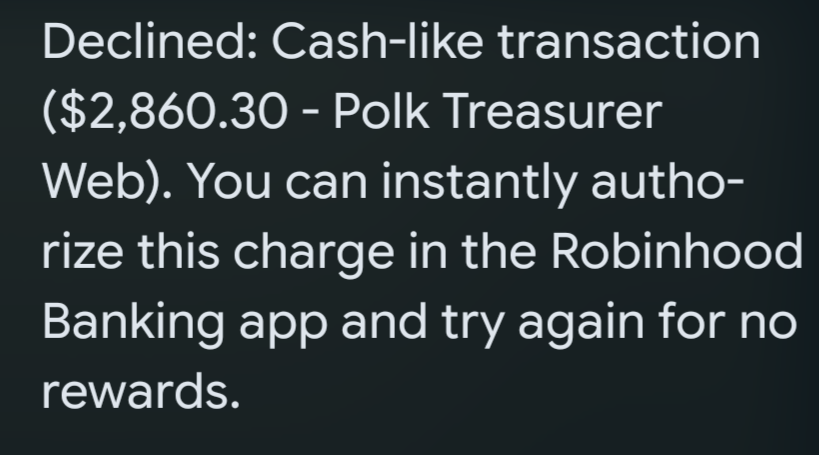

I tried paying my property taxes with my Robinhood credit card since the credit card convenience fee was less than 3%, but the transaction was rejected and Robin Hood said if I wanted to go through it that since it was a cash-like transaction I would have to agree to not get rewards and obviously that’s a deal-breaker. I’m sure I’ll score lots of good 3%, but I just thought I’d let you know about this awkward exception