Eh, could have put this in another thread but maybe worth starting a new one. Has anyone gone down this rabbit hole? I’ve been using a spreadsheet to track things, but it is pretty basic and I made it mostly just to track assets with a really simple projection into the future.

But I’m getting to the point I need to sharpen my pencil, and think about things like taxes in retirement, and I’ve never really factored in SS but I think it’s safe to assume I’ll get something there. So I’ve just started looking at some of the options, watched a couple of videos.

It looks like the most common ones are Boldin and Projection Lab, with Empower also pretty well-liked (and free, the others are like $10/mo if you want full access). Boldin looks to have a clean UI and it walks you through the setup, but isn’t quite as flexible as PL. I also see that Boldin uses a Monte Carlo approach for future returns, but I don’t see the methodology - are returns correlated between years, or are returns lower when the P/E is high, etc? PL uses historical data to estimate future returns, which I kinda like. I haven’t played with PL yet, I’m told it’s a little more work to set up but offers more flexibility.

At any rate, appreciate any thoughts and feedback from folks who’ve explored these tools.

will you have a big-ish to big pile of assets when you retire? assuming yes, a spreadsheet will work fine.

i’ve tracked my portfolio almost every trading day for decades. a few years before retirement i started forecasting annual expenses in retirement. i wasn’t too far off and we have more than enough resources to fund them. i care nothing about 30 year monte carlo simulations in retirement.

i considered the specialized software approach, looked at some, and decided against it. i was surprised to discover upon entering retirement that i just didn’t care much about those forecasts.

yes, it’s a valuable exercise to do the tax planning and structure your assets accordingly, but you can do the basics in a spreadsheet

have fun playing with all that stuff, but you’ll probably be fine with a spreadsheet and simplified assumptions.

It’s mostly this, yeah. The simulation models are fun. That said, the 4% rule is obviously pretty conservative. Plus I don’t think my wife and I will stop working 100%, I think we’ll continue to have some income to push the withdrawal rates lower. Plus I’m already targeting a reasonably fat budget, so if needed we could trim the travel, for example. So I’m pretty confident if I hit our number, we’ll be pretty well covered, but I’d like to play with these tools just to see what they say, and fiddle with some scenarios.

Oh, and I’d like to get a better handle on taxes, and these tools do that. I hate taxes and I’d rather just pay the $10/mo vs trying to build it all out.

FWIW, I’m currently targeting at least $3M, maybe more like $3.5M, plus a paid-for house. Oh, and at some point we’ll downsize and likely that’ll leave us with some added cash. There is a lot of conservatism baked into the plan. Shocking, a conservative actuary!

I’m thinking it depends on how complex you want to make it.

I’d do it in R (though I stuck my mortgage stuff in Excel), but I’m sure there are 50+ other languages you could do it in. Ask AI to help you with the coding.

Would taxation interact with your investment returns?

If you wanted to get more complex, partition y so that you have equities and fixed income and the different tax rates for those. Maybe you have multiple growth rates, one for fixed income, one for dividend returns, one for equities, and separate tax rates for each. You can make this as simple or complex as you want, but maybe you find out that the extra detail isn’t that useful on parts of it but is in other places.

Totally agree here with my almost two years in. As much as I enjoy minimally tracking this, that, and the other thing on a spreadsheet, I really don’t stress out about taxes or anything at all.

Things to consider:

If you retire early, you have to adjust your SS downward for the years you don’t work when it thinks you will. For me that is only about a 4% decrease (if you have an account it is very easy to type this in and find out) but it could be more for you.

If your AGI is over 82K (after 32.6K std deduction) you won’t get any ACA tax credits. How much Roth and investment account money will you have on hand / decide to use to keep your taxable income lower until you are 65 and on Medicare (and before taking money out of retirement accounts early becomes a hassle)?

What other adjustments will you have tax-wise? Lots of interest? Short term capital gains? Nonqualified dividends? Each additional dollar is income but also more taxes and maybe less benefit.

I don’t track expenses but I’m not a big spender. Even if you haven’t seriously tracked it I think you will inherently be able to estimate your spend and you will have reserves and you’ll be fine.

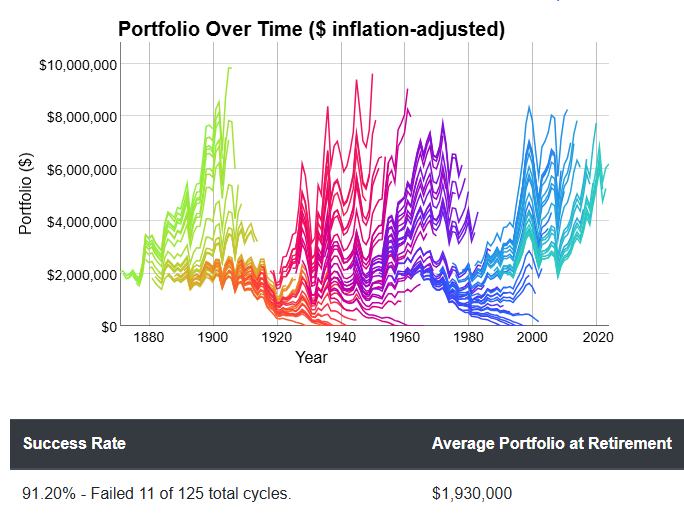

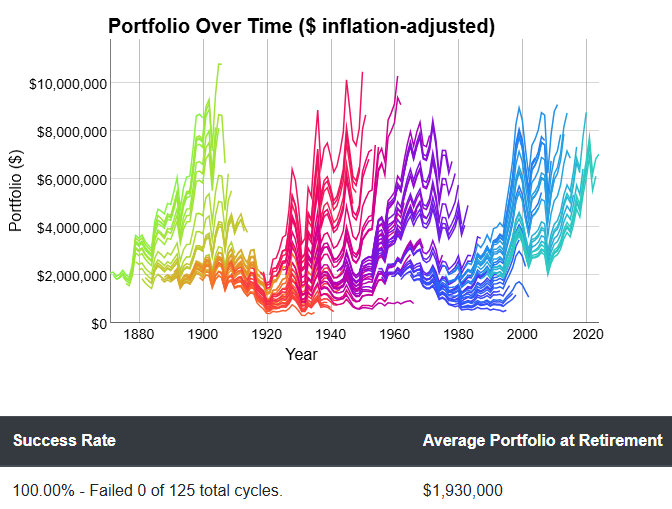

I went to cFireSim and entered my amount my SS and my investment mix and put in $85K-90K of annual spending and it said I would be fine using 100% of the previous 30-yr or 40-yr investment returns. That’s an easy site to play with to show you ranges of where your money might end up down the road. Of course who knows what the returns will look like going forward….

Yeah, I’d just be happy to see it with current tax laws. It kind of breaks my brain to think about cap gains, income tax, state tax, while trying to make sure I’m eligible for ACA subsidies.

I’m pretty sure we will be totally fine, if we get $10k/month in today’s dollars and the house is paid for… like, figure it out, man.

I have Empower set up. I only used it for a couple retirement projections. I think that it’s good for that but it’s not really a budgeting app.

I’ve really only done Gross Budgeting (Spending=Income - Net Savings). My credit union and a couple of my credit cards do a good job of categorizing expenses, if I ran all the payments through those channels I could just dump everything to a spreadsheet for a detailed budget tracker.