This is nice, I have a similar amount, and can buy up some additional time. But I struggle to use them. Its 3 weeks more than my SO, who also needs to burn some PTO each year for kids appoints, so its a challange for us to spend more than a couple weeks of this on family vacations.

I’ve added an extra week or two the last few years to visit a couple friends abroad. Without a destination though, it feels difficult to get away and use them just to burn some days off.

Obviously as a SAHD my husband is the one to handle appointments by default. I often attend them, too, but sometimes it doesn’t work out. Also my leaders don’t think medical appointments are a reason to take PTO, unless they are recurring or require a half day of time. So I’m pretty lucky.

If we both worked, the one with availability and PTO (if applicable for his hypothetical job) would handle them. That would likely be me.

Yeah, I’ve heard so many stories about people catching heat for retiring early. Friends, family, internet strangers. I have a handful of friends I’d tell, most of them are in the same socioeconomic class as us. Other than that select group, I’ll either lie about working or just say that I have a career in asset management (just one client, real jerk!).

If you go to the FIRE subreddit, there’s a tradition that when someone retires, everyone says: congratulations, and go f*** yourself.

I’d like to see the starting points they had for this.

Fully paid-off college education? Yeah, two DINK earners can be retired by 35 if they’re frugal. That’s arithmetic. Those who aren’t willing to do it will get mad but they either spent their money elsewhere or earned less is all.

If they started off with $50k in student loans or no college degree, that’s very impressive.

Some of these stories are like, “I earned $1M by age 26 and all I did was take the house my parents bought me, rented it out, lived with my parents while working/investing, and mooched off of them.”

My boss has been making more money than me for a number of years and is presently aged about 12 years past where I plan to retire, and plans “to be here for a long time.”

I haven’t mentioned my plans for an earlier retirement, but it will be interesting if I beat him there.

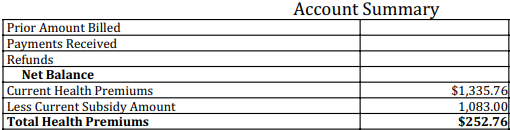

I’m not paying much every month, although this needs to reconciled at tax time (form 8962). My AGI is currently up to 61,126 so I’ll have to cough up 6.06% = $3,704. The percentage maxes out at 8.5% at 80,852. I think I’ll end up somewhere in between. So I’m really paying about $400/mo for healthcare ultimately. It all depends on how much you bring in. If my income were 30k I wouldn’t be paying a dime.

It is true, the ACA could go away and I would have to spend more on healthcare. That’s a risk but I don’t think the big beautiful bill did anything about it and Medicare starts at 65 so every day the potential impact of that risk goes down. The only nuisance is that additional income gets taxed at an increasingly higher marginal rate but that’s fair if I’m going to get this kind of deal.

I like my coverage too. Gold coverage HMO specifically with the UnityPoint network which is large in Des Moines. $2k/$4K deductibles and reasonable co-pays, MUCH less out of pocket than the HDHPs I had during the last decade plus (although my expenses were next to nothing). This is just for my wife and I who are 55 & under.

And a lot of people in early retirement will pull heavily from Roth vehicles, reclassifying as much Traditional as Roth as possible while income is low, while keeping under the MAGI threshold for the max subsidy.

Yes if I do draw money I will be incentivized to take Roth money until Medicare. Wouldn’t reclassifying from Traditional to Roth still generate taxable income? I mean yes you may as well hit the 30K cap if you aren’t generating income but that’s not a very large amount. You might decide the taxes are low enough that 40K or 50K is worth doing. Once you hit 80k you are looking at 12% federal plus 8.5% ACA = 20.5% maybe that is still attractive? (I never made FCAS money)

There’s a local politician here who is strongly against doctors and nurses retiring before age 65. He suggests it’s immoral because it reduces access to medical care for people and harms their patients (we have a doctor shortage in the province).

I think it’s mostly a lot of the province is highly unattractive to new doctors due to a combination of being relatively isolated, small, insular communities, distance from amenities, poor shopping opportunities and high competition for doctors everywhere right now.

If I was a doctor, I’m not sure that you could pay me enough to live in many of these communities.