i believe, if retiring and your income will he reduced, you can appeal the charge

1 Like

Yes

This is crazy … how long before the market takes some of it back?

Be on the lookout for a Double Dr. Evil if this keeps up

3 Likes

When you’ve won the game, quit playing. Take your chips and go home.

I’m not convinced I’m playing a game. Central banks seem to have an insatiable appetite for gold. Poland said they are going to buy 150 tons to get up to 700. I’ll happily pull back on a moment’s notice and scale back from 20% to 10% or 5% or whatever and I’m not under any delusions that I’m going to accurately call any sort of top.

I really didn’t expect to be double-dr-evil two hours after that other post! So far indications are another +10K tomorrow although futures have a way of changing when the market actually opens.

I do wish I knew how much of this is Central banks and how much of it is world/Trump uncertainty.

| 37.7% | International |

|---|---|

| 19.7% | Gold/Silver/Mining |

| 9.0% | Covered Call |

| 6.6% | Domestic |

| …. |

2 Likes

So what you’re saying is column 3 should be named “mark it zero”

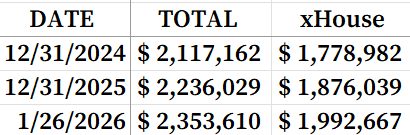

US Wealth:

Investments >>> House Value

UK Wealth

House Value >>> Investments

So what kind of property tax is there in the UK? For liquidity purposes, you’d have to have investments producing at least as much income as property tax costs, right? That’s not even counting maintenance requirements.

US Property taxes are way higher than UK Council tax.

A £1.5M house in London for example would be paying only £5k/year (0.003% of value)

The main property cost in the UK is stamp duty (a truly stupid property tax) which is born by the buyer.

For a £1.5m house in England/NI (standard rates, not first-time buyer/additional property), Stamp Duty Land Tax (SDLT) is £71,250, calculated with increasing rates: 0% up to £125k, 2% on £125k-£250k, 5% on £250k-£925k, and 10% on the portion from £925,001 to £1.5m, with rates increasing for additional homes or non-UK residents.

There is no capital gains tax on the sale of your main residence as well.

I cleared 2x in my vested balances, excluding the house. I should hit 3x TNW by the end of the year IF the markets have an average year. This is practically doubled in the last 2.5 years. The snow is balling.

I suppose you could consider this front loading property tax, but it has the impact of suppressing property turnover, and shifting the burden to new purchasers.

I live in one of the lowest property tax states, and I pay a rate more than double the council tax on my primary residence (and higher on non-primary).

What I’m really saying here is: If you have massive gains, take some risk off the table.

1 Like

Same in Canada in cities like Vancouver and Toronto.

Its not Central Banks driving the price anymore.

Its leverage. Gold price is now being debt-fueled which makes it very likely that the correction downwards (eventually) will be very fast.

Can you go into more detail? Why exactly is it causing the price to skyrocket now, and why would the price suddenly drop? Debt isn’t going to magically disappear is it?

GAIIIIINZZZZ!!!

GAAAAAAIIINNNNZZZZZZZ!!!

2 Likes

Margin trading using futures contracts.

There is no chance this type of growth in volume of contracts is not driving the price up.

I guess I’ll back down toward a 15% allocation…

….aaaaand it’s gone! (sold almost all my gold around $5,200-$5,250)

2 Likes