The run up in tech stocks has been good. makes me think a crash is coming. But our net worth has gone up quite a bit the last few years and most of it is unrealized capital gains.

The taxable investment accounts are now worth quite a bit more than our house which is paid off and pre-tax retirement funds we have in various accounts is around the house value maybe a bit more.

For the longest time home equity was the single largest bucket we had, that’s no longer the case.

On top of it, wife has a DB plan that will probably be close to 100% of pay when she retires and she still wonders if we have enough to retire. I told her if we can’t afford to retire early, America is trouble.

My wife also has one of those. I have had to explain to her how valuable those are when you can retire at 52 on a full gold-plated DB pension (thats a notional pot in the $3M range at $100k/year).

I find that well-off people often think they don’t have enough to retire whereas they do. After I turned 58, I figured there was no financial need to work longer but few of my contemporaries shared that sentiment.

Looks like your future kids will be millionaires by the time they are 18 with these Trump accounts: must be assuming some pretty optimistic investment returns.

The article says they project $1,000 to grow to anywhere between $3,000 to $13,800 after 18 years without any additional contributions. The IRR calculation is left as an exercise for the interested reader.

Anyone figured out what the incentive is for the donors? Who are the beneficiaries, and under what terms are funds collectible/surrendered? Somehow the donors are going to make money off this. Because literally every policy under this administration requires it.

Seems like there are any number of ways in which a company might want to be ingratiated to Trump. He’s been in the business of using government to pick winners and losers.

Dell might see some harmful tariffs lifted, or have the government invest in the company, etc. Never bad to have the ruler’s favor.

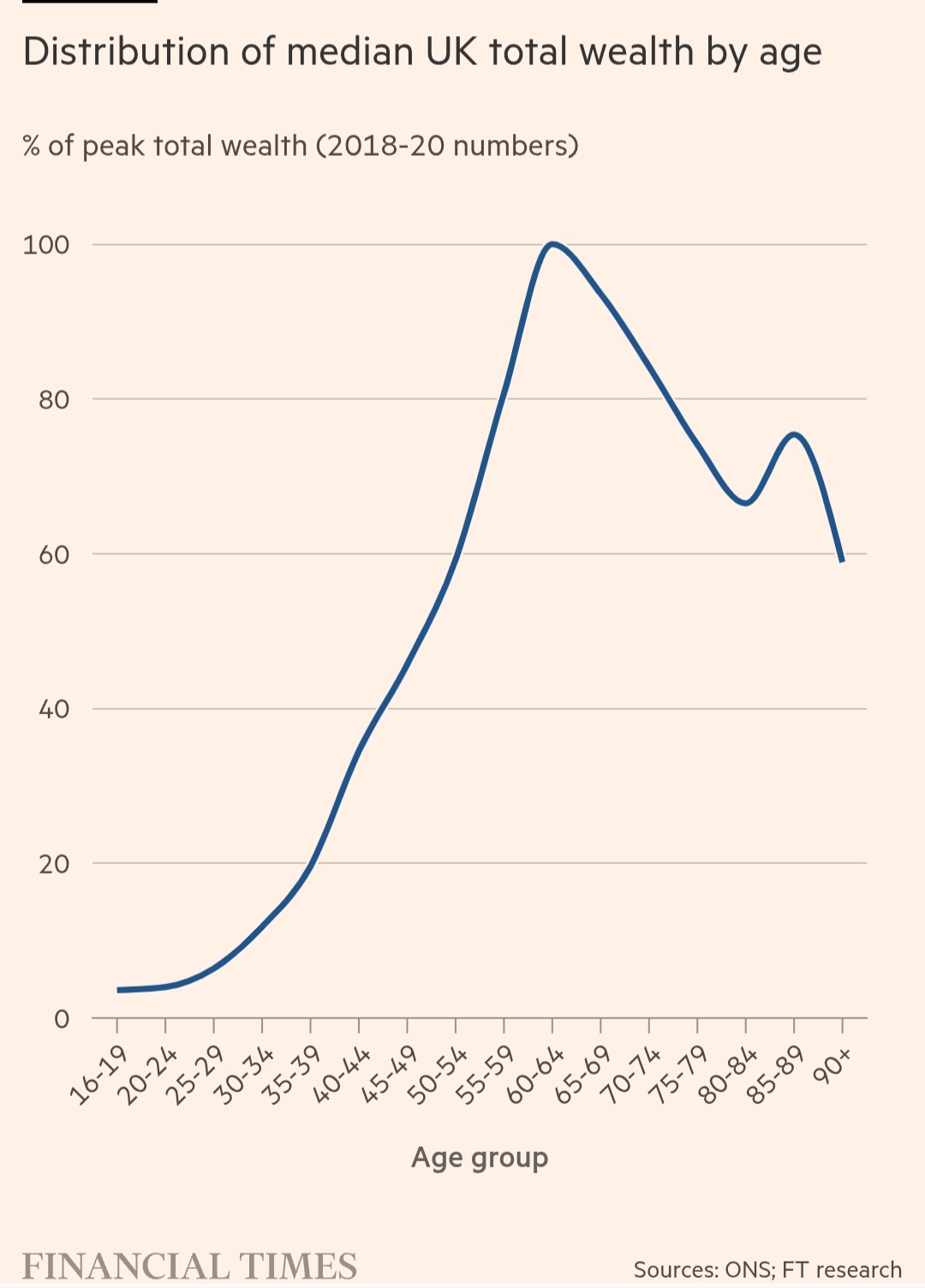

Have been looking at long-term retirement planning and found this UK-based median wealth graph based on age which is very interesting.

Median wealth peaks at around retirement age (this one is not surprising) But what is interesting is how little wealth deccumulation there is after that.

Retired people keep saving more instead of spending (leading to that bump in their 80s)

Could be related to care fees (scared of running out of money) but this looks much more behavioral to me (they got used to saving and accumulating so can’t really switch mentally to spending it down)

Could also be what the 50th percentile scenario looks like in a retirement simulation when your retirement assets are at a level to provide income at 90%+ certainty. Or, to be more precise, what the real world scenario of the last decade translated into.

I know both my parents have more in their investment accounts than at retirement. In recent years, the stock market has been very generous to retirees with gains exceeding their withdrawals. I’m afraid it’s leading to unrealistic expectations given how long it’s been since we saw a very lengthy period of time where it took the DOW, etc. to recover to a previous high.

ETA: also take a look at what house prices have done over the last several years.

My dad retired at 54.5. My mom went from PT to FT around then working for city hall - she had over 20 years PT, but since most of those years hit the 1000 hour threshold qualified for the state’s pension fund for municipal workers. That all worked out (with the FT average final salary) to have a really nice pension at retirement and that all materialized after my dad had retired.

So at 55 they had a paid off house, high 6 figures in retirement savings, my mom working FT. At 65 they had SS income and sweet pension that more than covers their expenses. You could imagine what 20+ years of that savings growth and inheritance from their parents might look like today. Way more than they will ever spend.

Our balance is much higher than when we retired, but we retired Q1 2020 so right into the teeth of C19 and a down market. And that’s after several international trips including a luxury trip, large charitable gifts, a new car, etc. IRMAA sucks though.

And it’s not like we have a super aggressive or speculative portfolio either. Mainly dividend payers, broad market index funds, TIPS, etc.

2026 will be our first full year on SS (started at FRA) and it’s enough for the gotta have stuff. Drawdowns pay for lifestyle.

Looking forward to QCD eligibility.

edit: I’ve tracked our portfolio balance almost every trading day for decades and I’m immune to the wild market swings and unrealistic expectations. I know that a crash is coming. I also know that a boom is coming. It’s the timing that I don’t know.

Once we turn 70.5 we can make charitable gifts directly from our IRAs to the recipient. The gift doesn’t flow through the tax return as gross income and therefore reduces the IRMAA impact.