I added the fed funds rate to the IORB graph and saw that they overlay nicely. That makes sense to me as the second seems to be the direct method the Fed would use to control the first.

I also noticed that these rates went up sharply in 2022 when the news stories said the Fed was raising interest rates “to fight inflation”.

It seems that if the federal gov’t decided to control its interest expense by only issuing only 3 month bills, then having the Fed keep these short rates low, the Fed is stuck in a situation where it can’t use interest rates as an inflation control tool.

And, those primary banks would have to find customers who want to invest/save money for short periods at very low interest rates.

Good point. Believe it or not, there is an active market in decomposed Treasury securities.

A bond’s cash flow can be separated into 2 distinct pieces: the semi annual coupons and the maturity value. So take a 10 year bond. The bond itself has a duration in the neighborhood of 6.5 or so. The maturity only portion, is priced at the spot rate and is casually referred to as a bullet. The bullet has a duration of 10.

Each of the two synthetic credit instruments has a market. Often for hedging purposes.

Ummm. Same clients that bought the 3 monthlast time?

Fed can definitely issue longer dated one. Just keep the coupon low, like 1%. Won’t need many, since the bank reserves can absorb the new debt issues. They have so far, so I don’t see why that changes.

The lower coupon…well that will translate to lower cash flow sent to bond holders. As I understand it, the only thing that affects the deficit is those interest payments. The Fed doesn’t mark outstanding bonds to market on the government’s books. No real amortization or depreciation on assets passes thru to the deficit. So it never affects the national Debt. Which circles back to my assertion that the value of the debt is meaningless. It’s just a number

My original understanding was that you would stop issuing long bonds and do all borrowing in maturities where the Fed can control interest rates. That means a lot more than bought last time.

But this says that they would still issue longer maturities, just with lower coupons. So they are all issued at discounts.

I understand that the federal gov’t does not book amortization of discount on a monthly or quarterly basis. But, Google tells me that for bills, which are currently sold at discounts, the difference between the selling price and the maturity price goes through “interest” when the bill matures. I assume we would do the same with longer maturities if we sold them at discounts.

I think that the amortization would hit the reported interest, deficit, and debt, the timing would be somewhat different. And, if you are concerned that wealthy people are the beneficiaries of interest paying debt, that wouldn’t change, they would still take more cash out than they paid in.

I don’t get this comment. I see total bank reserves at $3.3 trillion, which is a lot less than the federal debt.

By lowering the coupon rate you will reduce the interest expense but you will increase the amount of debt. Lets assume the 30 year rate is 4% and the bond has a 1% coupon rate. It will sell for about half of the face value. To raise $100 you have to sell bonds with face amount $200. Your interest expense has declined from $4 to $2 but you have doubled the amount of debt. Lower deficit but higher debt.

Why not just have the issuance of 0 coupon bonds, and avoid the need for the creation of STRPS.

I assume this is not true. The treasury auctions for primary dealers do not require all bids be at par. They can be either above or below par. They are just the high bids.

The comment on bank reserves can absorb… here I am trying to address phrases I see about..“No one will buy the bonds when the deficit is this high”.

The Fed is more agile than that. In 2008, in response to that meltdown, the Fed started a program whereby they would lend the money to the primary dealers to purchase the new issues. Sort of like the discount window (lender of last resort?) that has since been discontinued, but it’s a historic fact that they did so. The Fed supplied the liquidity.

I’m assuming that the plan is to sell them at very low coupons. If so, then I’d expect all the bids to be less than par – at a discount.

Eventually, the gov’t pays the par amount. The revenue from the sale and the payment of par value both have to be in an accounting statement. So I’m assuming they label the difference “interest”.

I don’t know if the label matters here. The economic fact is that the lenders got more dollars back than they paid in.

I can believe that. I also assume that is a rare response to an extreme situation. I wouldn’t treat it as an routine practice.

Indeed, to accretion seems to pass thru the balance sheet. The accounting gets really arcane with all the intragovernment crap ( bonds in the SS account),

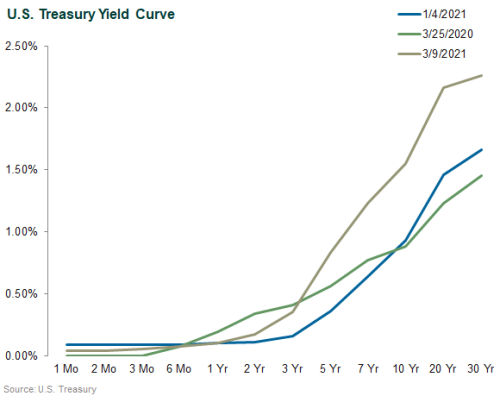

It’s worth taking a look at what the yield curve looked like in a very low Fed rate environment. We just had one.

The longer dated bonds do exhibit a term premium, but the interest cost is a heckuva lot less. I still maintain the interest on the debt would be reduced.

I can believe “decreased”. I think the term premium is driven by fundamentals outside the government and is likely very persistent.

I also think “supply and demand impacts price” is a fundamental thing. If the Treasury is trying to cover all Federal borrowing with very short bonds they may discover that the Fed can’t put cap on short term interest rates and also find private lenders willing to lend at that price in the volumes they need.

Fundamental…but do you accept the definition of a monopoly..that only the seller gets to set the price? If I owned the Mona Lisa, there is no market price. The price is whatever I say it is.

I guess I don’t. I accept the definition of a monopoly … “there is only one potential seller.”

Classic monopolist pricing assumes a demand curve. Some people simply won’t buy at certain prices. If you want to accomplish an actual sale, you can’t name just any price.

The US Treasury can say that the only way they borrow money is with 3-month bills. They can also set a price that equates to an effective yield is 2% (or whatever). But, I don’t see a way to force anybody to buy at that yield. More relevant, I don’t see a way to entice enough people to buy at that yield. You are seeing some mechanism that I’m missing.

Mostly true, but it depends on the item in question. If it’s a necessity, then sometimes people have no choice but to buy. If there was only one provider of food, for example, they could theoretically charge whatever they wanted, and people would have no choice but to buy it.

My limited experience with fine art is that it’s often sold at auction and the market determines the price, though the seller may set a reserve price. Presumably that would be the best way of selling it to maximize the price you get for it.

The mechanism is coercive force. The only way to pay your taxes is to transfer U$D. You cannot settle your tax obligations with a wonderfully crafted sofa, or bushels of corn, or even gold. It has to be $. If you do not pay your taxes, you will be put in jail. Make no mistake, you cannot decide to not participate. You must collect $s.

At some juncture, this fact must be included in anyone’s concept of what “money” is. The purpose of a sovereign currency is to facilitate taxation.

Archeologists routinely find ancient coins in Roman ruins in Britain, Turkey, North Africa, and the Balkans. Why? Because those were Roman territories and the inhabitants had to pay taxes to Rome. They acquired those coins by sending real resources to Rome - wheat, olive oil, furs, etc. to acquire the tokens they needed to pay taxes. The traditional story about money was that it was invented to facilitate trade. That was false. It was pure fiction.turn. The physical evidence is irrefutable..

I’d think for a lot of trade coins would be a lot more convenient than transporting bulky goods back to wherever you lived. Presumably a lot of people want to earn a profit on whatever they’re trading and they don’t necessarily want to spend all their profit at once. So you’d need something like coins to cover your excess earnings (e.g. the portion of the trade value that you don’t want in goods).

Also, I’ve been listening to some medieval history podcasts recently and they mention these giant barns/storage buildings that were used in what is now the UK for collecting the trade goods the church or local government took in as taxes.

So perhaps the history of currency isn’t so clear cut.

Like sharecroppers. The lord of the manor didn’t have a sovereign currency, so the serfs turned over portions of their harvest. Gotta store it, I guess.

It didn’t start off that way in pre-Roman times (think Ancient Mesopotomia), the Romans (really the nobility and upper strata) just ended up adjusting it for their own purposes (and advantage).

The phrase Render unto Caesar stems from their use of money and taxes.

Yup.

I was impressed with David Graeber’s book on debt. He is an anthropologist, not an economist.

The trad story of money is really from 18th and19th century economists. It’s a narrative, not a scientifically supported fact. https://en.wikipedia.org/wiki/Debt:_The_First_5,000_Years

I found it fascinating. A compelling argument that debt came first and then came money. Sort of the reverse of the trad story.