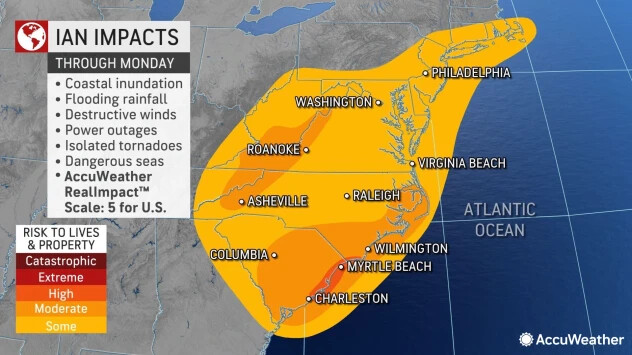

“Hurricane Ian will forever change the real estate industry and city infrastructure. Insurers will go into bankruptcy, homeowners will be forced into delinquency and insurance will become less accessible in regions like Florida,” he said.

We probably have people on this board who could add some professional insight…

Hurricane Ian might be the latest impetus for the state regulators to actually allow companies to charge appropriate rates; but Hurricane Andrew holds the claim of “initiating” such changes. But it’s clear that the FL politicians either have short memories or generally don’t care about history.

What is likely to happen is that (modern) building code will be more strictly enforced; with the impact that many homeowners may not be able to afford rebuilding their homes to be “the same” pre-hurricance . . . especially if their abode was “grandfathered” in to the new building codes.

Very likely that many of the “stand alone” companies are likely to go into receivership and the industry picking up paying the remaining claims. Might consider what happened in 2009 with a major carrier in FL.

Not sure what population you’re drawing on . . . but there are quite a lot of insurers writing property insurance in FL. However, most “major” insurance companies will have a FL-specific subsidiary.

During the early part of 2010’s, Citizens (FL property insurance residual market company run by the state) was the #1 insurer in the state.

Unless you have a “wind exclusion” on your policy, your HO policy should cover damage due to the wind. (Think what would be covered from a tornado.)

Often, what the challenge is whether or not the damage was done by the wind (and subsequent water damage is part of the claim) and what damage was done by flooding (usually excluded; can be covered by a flood insurance policy, though).

But JSM does make a good point around whether or not the solar panels were considered in the establishment of your insured value.

FL insurance commissioner is an elected politician . . . so the direction they have typically followed is to not allow increases to rates–especially for the larger insurers.

If a company cannot charge a rate that will keep them solvent, they’re going to start limiting their exposures by starting with the most risky ones.