Property tax is the other big one I can think that you may be missing, if your insurances and other major purchases all run through your CC and not bank EFTs.

Rather than trying to accumulate my cards, I just went directly to my bank accounts and added up every single withdrawal that wasn’t investments, income tax payment, etc. Including credit card payments. Everything that is actually a spend, basically.

Based on what you have shared here, I am guessing you are way undershooting where you will be. I look at my own projections now and 3M (ex house) by age 50 and 5M by 55 are starting to look more likely. Each successive +1M takes about half as long as the prior one.

Yeah, I’m starting to consider the possibility of earlier retirement than I’d previously thought. As I got more into FIRE (Financial Independence Retire Early) concepts I thought of it less as what age I might retire and more the number required.

I have never believed that the value of one’s primary residence should count towards the definition of being a millionaire but the UBS 2025 Global Wealth Report seems to. Especially inappropriate for Canada where the average Canadian household net worth exceeds $1 million including home values.

Surprised that Gen X, rather than the Boomers, has the highest real estate wealth in Canada. Don’t know if this is true for the US as well?

Australia, like Canada, has the absurd situation of being a low density country with very high house prices. I’m guessing the main reason is that people need to live close to work and the bulk of the jobs are located in a small number of cities.

I was hoping that remote/hybrid work would stick around after COVID so that people could live further from work but it looks like most companies are going back to full time onsite.

I’ve started to pencil out expenses a little bit, with no mortgage I think we tend to spend about $80k. Don’t get me started on home renovations, I’ve spent $75k+ in the past twelve months.

This will be the last year we spend this kind of money for sure. I have some other things to do but more like $25k/yr for a few more years, then less. Eventually something will come up but the roof and HVAC are near new, so it shouldn’t be crazy for a while.

I’ve factored in property taxes and insurance in my $80k swag. And that includes some padding for auto repair and some vacation money but we probably want more of the latter. So I’m probably not going to feel too solid until we get to about $100k of income plus a paid-for house. That’s probably when I stop caring, and I may or may not coast until I’m north of that.

The Federal gov’t here (Canada) is talking about having to cut spending by 15 to 30% depending on whether the cuts are cumulative or aggregate. We also got an email from the top public servant discussing the need for innovative solutions. Lots of comments from public servants about how the gov’t was talking about all the money they could save with more remote work/wfh. The stupid plan we ended up with in RTO v. 2 or 3 was a minimum of 3 days a week in office. High enough that they don’t cut space demand enough to downsize office space. If they could have gone with 2 days, they could have compressed more.

I don’t like how the tax rate is implemented. I think it is wrong.

If my effective tax rate (ETR) is 10%, then the portion that I keep is 90%.

If I want to spend 100,000, then I need to make 111,111 in order to net 100,000. The model doesn’t divide by (1-ETR). Instead it multiplies by (1+ETR) which understates the amount required. It tells me I need 110,000 in order to spend 100,000, which is not correct IMHO.

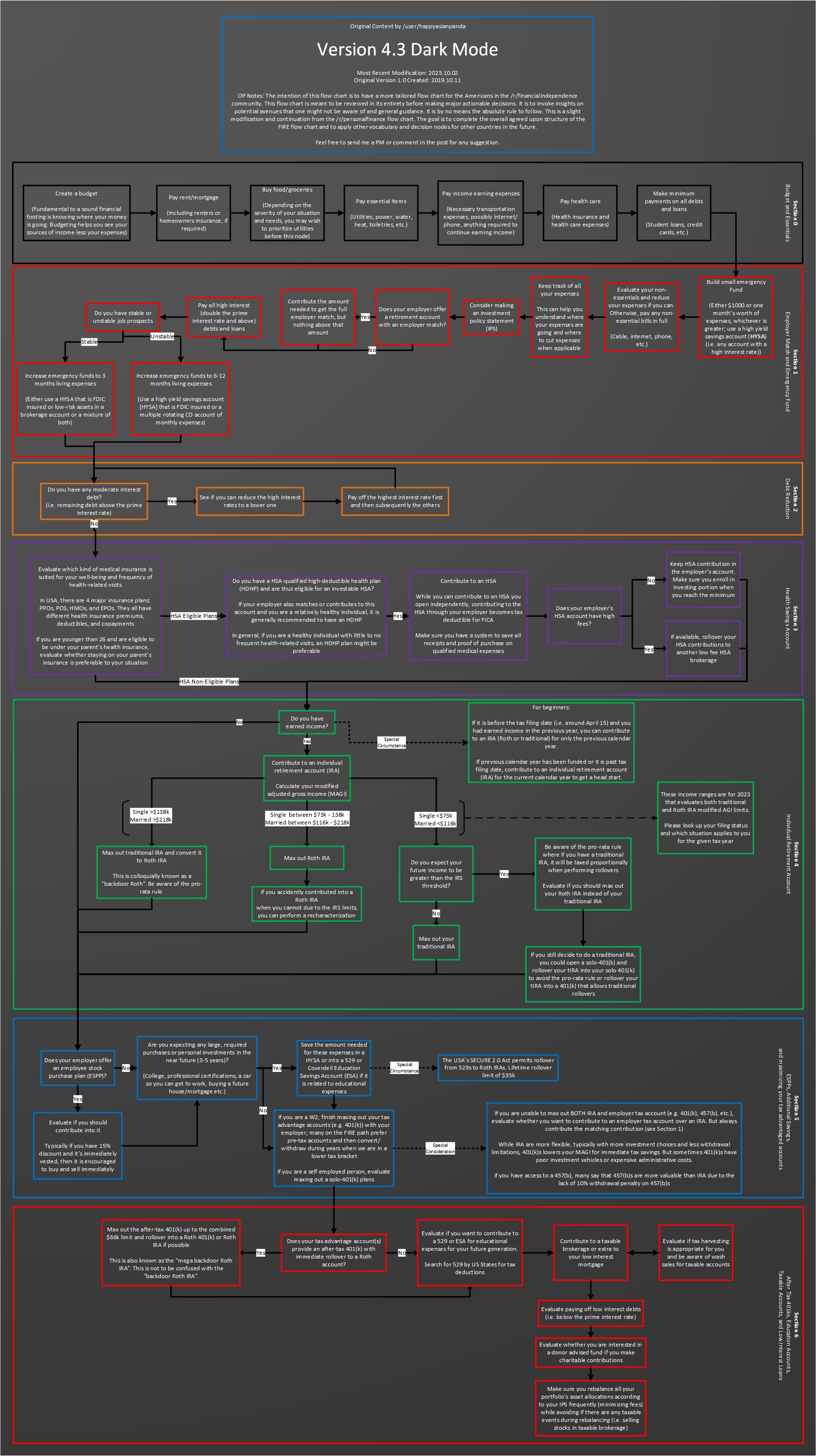

I didn’t closely review every step because some aren’t relevant to me, but it seems like a pretty solid update. For example, it touches on the trap of keeping funds in a Trad IRA if you wanted to do a Backdoor Roth IRA.

It seems to miss proper planning on how to access your funds early, though.

{kind=link}