obligatory Simpsons gif

I finally have 12 months of data from 11/1/2024 - 10/31/2025.

Savings rate of 48.0%. A bit more than I thought, actually.

I know it’s hard to define savings rate with taxes and all that, I think as long as you’re consistent this is a good directional type of metric. 48% is pretty bonkers, nice job!

In the past I’ve looked at my W2 and used that as a proxy for net income as the denominator in my estimated savings rate. I hit >50% in 2019, and then we bought an old house, lol. I was more like 35% for a while, I think for 2026 I’ll be in the mid 40s.

I’m defining as: (Money into 401k/HSA/IRA/brokerage) / (Gross income). Would exclude mortgage overpayments, but those were minimal this year.

Need a thread for 2026 @tommie.frazier

Looks like 2026 401K catchup may impact a lot of us

come on, it’s still november!

agree on the catch-up. will still do it, but yeah it will be stuffed into a roth.

I have a few stocks in my taxable account that i could sell right now and generate a 3k net loss for the year. I should recover about 40% of that in taxes. This is a no brainer, right? I could buy it back in early January if i want to keep the investment.

Risk - lose out on a recovery of the stock. I could buy into a competitor and bank on any industry news correlating.

Just make sure enough time elapses that the IRS doesn’t consider it a wash sale.

30 days… i think based on the date it settles rather than the day i push the buttons.

Are you able to deduct capital losses from your taxable income even if you have no capital gains as an offset? Our tax system only permits capital loss deductions to the extent they are offset by gains but we are able to carry forward capital losses indefinitely or back for three years.

We also have a “30 day rule” for acceptable tax loss selling and repurchasing.

"You can deduct capital losses from ordinary income up to a maximum of $3,000 per year ($1,500 if married filing separately), but only after first using your losses to offset any capital gains. " from the AI

There is also a rule that you need to use short term losses to offset long term gains, even though the gains have favorable

Tax treatment. So it seems to be beneficial at the end of the tax to harvest the tax loss when it can be used to offset ordinary income.

I have a simple rule about taking capitol losses here: take them as soon as you can as the rules around them have changed so often over the decades and could change unfavourably again.

Most of my investments are sheltered in IRA accounts so I only trade them based on how I see the companies performing. For my brokerage account investments, I’ll take any losses that I regard as meaningful. I’m finding that as I go on I have very few positions in a loss position.

The maximum amount you can deduct in a given year is $3,000, but you can also carry forward losses. So if you are able to book a loss greater than $3,000 you could fill up your tax loss harvesting bucket for a few years.

I (un?)fortunately only have a couple positions that are in the red. I traded off the larger of the two this morning and picked up a net~7% on the movements since this morning…woot!

Well, I had some cost overruns on the house, and about $5k in unplanned medical spend. So, maxed out the 401k but only added about $41k to brokerage.

It’s fine, from here on out the home projects will be an order of magnitude cheaper than what we’ve been doing, so my savings rate will tick back up to normal-ish next year. I’m going to DIY a guest bath, and it’s going to be fancy but it’s such a small room, won’t spend more than about four grand.

Added 135k to the brokerage compared to my 100k target, although a bit of the excess is managing down my checking account and a bit is really delayed spending on new car. 2026 might be an expensive year, and that might be the start of a trend with college tuition looming on the horizon…I think I am covered but there is such a wide range in numbers its hard to be confident.

I found about 20k in home improvement projects to chase after. 9k or so on replacing HVAC #2 and the rest a few smaller DIY projects. No big purchases for year outside of those projects.

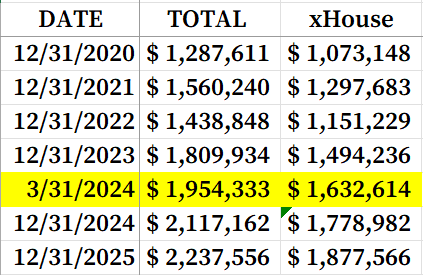

Starting to see the snowball effect in the brokerage. That alone is now throwing off enough dividends that it covers the interest, taxes, and insurance on my mortgage. I’m averaging about 4% on a 25% larger balance compared to the 3% I am paying on the mortgage.

2026…don’t expect nearly the same bonus, hopefully the car spending won’t exceed my 2025 home improvement spend, but 100k might be a stretch.