i have done that math too. part of the upside (to me) for some planned retirement job is to manage the hours (working) to a level that isn’t onerous but also to use it to manage the hours - how will i successfully and productively spend 16 waking hours every day? the upside is I won’t need it and can walk away if I don’t like or plan some time on the road or whatever.

i may have decided that substitute teacher is the easiest - always a need. can work whenever you choose (during school year). pay isn’t awful. etc. One to two days a week tops for me.

wanted to call out that I appreciate the explanations and figures you’ve shared. has helped me form my own plan and realize the biggest areas of improvement in that plan. unfortunately for me, I will be no where near walking away for enough years that my retirement won’t look too “early”

You’re welcome, I thought that many would enjoy some insights of real-life early retirement from the perspective of an actuary. My dad was able to retire as an electrical engineer in his late 50s and wasn’t a big spender but did lots of things he enjoyed such as scouting and occasional travel. Aiming for early retirement wasn’t a lifelong goal but I suppose the combination of having watched him and working in a good profession caused early retirement to come naturally - and earlier.

Yup. Each additional year is +4% for a delay in withdrawals and +10% from incremental savings. One or two more years can be a massive change in the picture. I could probably retire at 50 and be OK if I watch my expenses a bit, or I can work until 52 and pretty much never have to worry.

But it also comes down to how much I hate work at that point.

He was recommending this for people who were hitting 55-65 and just realized retirement was rapidly coming up and weren’t sure how to survive. It basically buys you more time to save, allow your retirement savings to grow.

How much more do you have to pay now for health insurance (compared to while working)? Also, did the 70K cover average expected home maintenance costs or could there be some big bills down the line?

Although my salary wasn’t mega, I had a lot of vacation and very low contribution to benefits. So I’m not going to try to compare to that. But the key to early retirement was definitely the ACA.

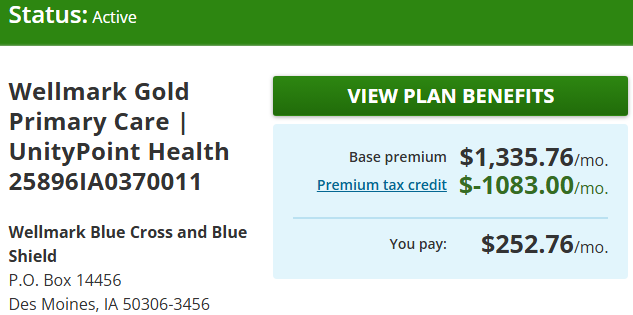

I currently “pay” $253/mo for an ACA gold plan. I’m in Des Moines and my plan specifically requires the Unitypoint network (which is huge). What I actually end up paying is determined when I do my taxes next year and reconcile the amount.

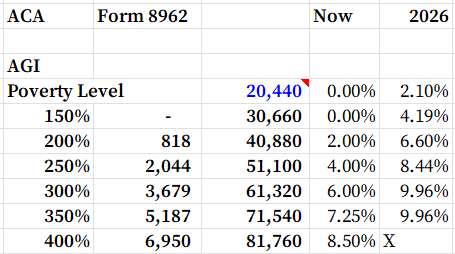

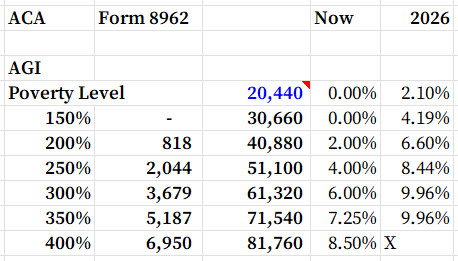

In 2025 anyone with an AGI below $30,660 can have free healthcare while those with an AGI of $81,760 will have to pay 8.5% = $6,950.

In 2026 thresholds will go up with inflation and the contributions will revert to a “normal” higher rate. Those with an AGI of $31,725 will pay 4.19% = $1,329 and those with an AGI of $84,600 (which is 400% of the federal poverty level) will pay 9.96% = $8,426. Also if you exceed that threshold you are no longer eligible and have to buy insurance elsewhere.

So it’s not super-expensive, but the gradually increasing tax rate also disincentivizes me from making money, particularly next year.

I thought of this route until I found out the cost of the liability insurance. I would have needed to do a lot of consulting for it to make sense financially.

Instead I took on public institute board and trustee positions where someone else provided the liability insurance AND provided a provincial government indemnity. That made it worthwhile even working just 200 hours per annum.

OK, but that math still isn’t mathing. The PV of 10k a year for 10 years @5% is 77k. It’s never “like having another 250k” unless you plan on earning 10k the rest of your life.

I’m hoping less liability is involved in the fish business vs. being an actuary. I was probably also a bit loose on my language. I’m basically looking at taking contract jobs with first nations or small countries helping them with stock assessments and getting their voices heard.

In the immediate year, it’s like having $250k to draw your $10k on. Yes, I agree, you would be better off longterm to have the $250k invested, but in the current year, your income isn’t that different from someone who has $250k in retirement. I think the expectation is that you’re going to have to work til you can’t work anymore and then go into a care home or sell assets.

In my first year of being a trustee on a large healthcare benefits trust, we were sued individually for millions of dollars. There was nothing like seeing my name on a lawsuit that reinforced my fears over liability.

i checked account balances of the 4 accounts and excluding home equity, we have eked over the thread title threshold. must have happened a couple months ago.

In my spreadsheet, i am ~6 months ahead of where I thought I would be based on a check at yr end last year. (so at 12/31/2024, I did not project to this balance until end of april 2026 but am here at 10/31/2025.)

eta - the main focus of my personal spreadsheet relates to actual spending and projecting that forward. hard to do with kids now (and in college) vs a future without extra mouths eating at home or on the payroll in general.

I’m setting a personal best for the number of sources of income this year.

$32,711 deferred income from Chubb which will pay out for another 4+ years.

$13,274 consulting income.

$11,700 from delivering for 3 companies: Uber, Instacart, and Spark (Walmart).

$5,650 teaching a 6-week online course for Drake University which I am halfway through as we speak.

$450 from tutoring, a fraction of previous years but I lowered my rate a bit and more is starting to trickle in. Helping students with their statistics homework in your basement is easy money.

Technically getting paid from 7 different companies.

Next year I’ll be directing 2-3 bridge games per week that will be $120-$200 per week. I go there and play like I already do and there is an extra hour or so of work. That is a pretty great work/play synergy there. I didn’t want to get tied down but another retired guy is doing half of the games so I can leave when I need to, and when he wants to take a trip I’ll do all five games for a week or two. (I can’t play in the two games he’ll be directing, so I’ll bring my French puzzle magazine with while I sit around for three hours)

I’m not bored, but as I’m not tied down most of the time I like to punctuate my life with these opportunities when the best offers present themselves. Getting out buying people’s groceries is exercise. I don’t know that any more actuarial work will come by, maybe I can find a place that designs Excel spreadsheets. FYI I’m not expensive if anyone needs anything. I would love to do some spreadsheet work but am not desperate to. Now excuse me while I try to figure out where to vacation in Europe next year.

The $1,100 premium tax credit is based on $40,000 of income next year. My income will likely be higher than that, but I’ll just pay more and that’s neither here nor there.

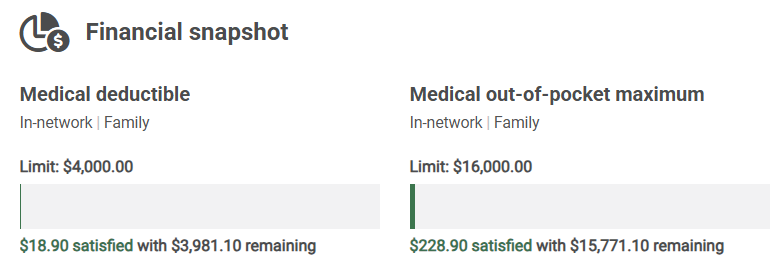

For 2026 I might dial back to the bronze plan. It involves going from a 4,600/16,000 ded/OOP to a 15,000/20,000 ded/OOP plus the copays are higher but that’s fairly negligible. In exchange I would save $3,444 and if I saved that each year for 1-3 years I would make up the difference in my deductible. Despite being 54 and minimally obese I have no reason to believe I’m going to start utilizing medical services.

It’s not a question as to whether there will be subsidies. It’s a question of them reverting back to pre-COVID levels. Based on the chart people should expect to pay anywhere between 1.5% and 4.4% of their income on top of the current levels.

If my income is 41K-51K, this year I would pay 2% of my income ($820-$1,020) but under the original ACA setup I would pay 6.6%-8.4% ($2,640-$4,284). I’m not sure the the website is accounting for that change yet. I’m not going to complain though, I will just pay it, since I am only paying a fraction of the list price, maybe 20%-30%.

But marginal self-employment earnings get taxed:

12.0% Federal

3.8% State

14.1% Self-employment tax

9.0% ACA tax (51.1K starts at 8.4% and soon maxes at 9.96% but I doubt I will hit that level).

TOTAL 38.9%

Some qualified business deductions still exist to offset a small portion of this.