Apples to apples is hard. The 4% rule assumes you have assets, and that those assets are invested in something like 75% equities and 25% bonds. That gives you about a 95% or so chance at making it 30+ years without going broke.

I think that perhaps it would be better modeled as an income stream. Let’s say you retire today and want a $50k income, growing with inflation. This year you get $10k from the annuity and draw $40k from assets. Next year you want to draw $51.5k, $10k plus $41.5k from assets. And so forth, over time the $10k becomes a smaller and smaller percent of your income.

Which is straying even further from a simple rule of thumb, admittedly.

Finally made an IRA contribution for the first time in a while. Roth IRA = Roth IRA + $6000.

Didn’t even realize the limit went up to $6000 recently. I slammed $5500 in for my first several years of working and let it sit for a decade, as I gradually worked up to maxing my 401k. The IRA is over $100k now. Living on a college lifestyle for a few years was a good plan.

Did you backdoor it? Most credentialed actuaries will be over the income threshold. Maybe not if you are an ASA working in the Po, are married, and your spouse doesn’t work. But most will.

I was also thinking of the Trad phaseout ($105,000) not the Roth phaseout ($198,000) when I wrote that. A lot more married GoA posters will be under $198k than $105k since many will be in that range of taxable wages.

Haha, that makes sense. I’ve never even considered Traditional anything, except a small rollover from a prior 401k from long ago. Yeh got me scared for a moment when I saw the Roth single income limit though!

new Civic EX in blue, yes I am. Hopefully I will take delivery of it this month after a 5-month wait. I won’t be getting it at a discount, but hopefully that will be offset by what I get for the existing one. My price was locked in when I talked to them in August, so if they want more now I shouldn’t be affected.

Would you mind sharing how much is new money each year and how much is growth? My accounts grew 105k from 12/31/2020 to 12/31/2021, which was ~56k new money, 49k growth.

Yeah, when Ranger mentioned a 26% CAGR, maybe it has grown that quickly but not from just investment returns. Generally I would have maxed out my 401K (about $25K) and two Roths (another $12K or so). Theoretically anything I don’t spend ends up in the investment column regardless of which account it ends up on (apart from college or home equity).

I think I’m going to take a break from putting money in my Roth’s now. I can just have it in my taxable investment account. Last year I was able to start deferring 15% of my income which is nice because it keeps the taxes low and will pay out in 5-7 annual installments when I leave the company. Not everyone typically has access to that. It’s sort of a forced early retirement, a way to bridge the time between age 55-57 and Social Security.

The amazing growth isn’t any sort of stock market expertise, it’s just trying to have a sensible portfolio, several consecutive good stock market years, and just living far below my means and not having too expensive hobbies (or getting the credit card companies to pay for your flights to Europe)

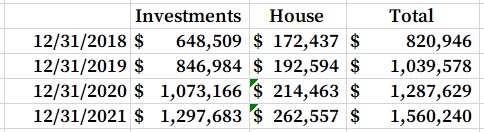

With a starting point of $1,073,166 I probably added $60K of my own money and then watched everything grow 21%. The S&P was up 26.9% last year, and my portfolio is a bit more conservative but <10% bonds still. And I’ve spent my entire career in the 'po on the far left of any salary band.

I’m curious how long you’ve been keeping track of this? I think you said somewhere in this thread, but it’s nearly 500 posts now and might’ve even been back on the Outpost.

I’m curious to wildly project my own numbers based on where I am, compared to an earlier point for you. Aiming for FIRE but not for over a decade.

Since 2009. I just keep it on a spreadsheet, all my assets (and my one liability, a mortgage) on a tab. I used to include my cars but no longer, since I’m not going to liquidate them to pay expenses. The $260K in my house is a bit too much to ignore though. I update it regularly, and at the end of the year it stays fixed and I put the new year on the line below.

It’s a good way to see how things change over time. At the end of 2009 I had $280K to my name. People probably make more later in their career, so it can be difficult to see the path to retirement from a long ways away, but it is fun to see the progress. Since 2009 my money has doubled about every 5 years, a combination of stock returns and income.

There is a tab for retirement forecasts. Take what you have now. Assume for each investment how much it will go up over time due to market returns, and also what you will contribute to it. Factor in your own salary and its increase over time. It’s not difficult to do, and nice to have a road map. Over time you can tinker with it and customize it to be more accurate to your situation.

Since 2017 my money made more money more than I did.

I’m looking forward to the point where my money makes more than I contribute, having it make more than I make seems like a pipe dream, but that is essentially the goal, it will just take a while to get there.